Certain items must be disclosed separately in the notes if it is material (significant). This could include items such as restructurings, discontinued operations, and disposals of investments or of property, plant and equipment. Irregular items are reported separately so that users can better predict future cash flows.

Why are operating items reported separately in the income statement?

Certain items must be reported separately from continuing operations on the income statement to provide transparent communication of the organization’s performance. These items can be misleading to financial statement users if they are not reported separately from income from continuing operations.

What are separately disclosed items?

A Unusual or Infrequent Item Disclosed Separately If material, they will be disclosed separately, before tax. Unusual or infrequent items are typically left in primary analysis because they relate to operations. In supplementary analysis, unusual or infrequent items should be removed net after tax.

How is discontinued operations reported on the income statement?

Discontinued operations are reported on the income statement separately from continuing operations. When companies merge, understanding which assets are being divested can give a clearer picture of how a company will make money in the future.

How are extraordinary items reported on the income statement?

Extraordinary items are included in the determination of periodic net income, but are disclosed separately (net of their tax effects) in the income statement below “Income from continuing operations”. As shown below, Anson reported the extraordinary items after reporting the loss from discontinued operations.

Where is a gain or loss from discontinued operations reported in the financial statements?

income statement

Income and expenses related to discontinued operations can be found on line items on a company’s income statement, below “Continuing Operations Income” and above “Net Income”.

Which of the following is included in comprehensive income?

Comprehensive income includes net income and unrealized income, such as unrealized gains or losses on hedge/derivative financial instruments and foreign currency transaction gains or losses. Comprehensive income provides a holistic view of a company’s income not fully captured on the income statement.

What are exceptional items in income statement?

Exceptional items are costly events that have an impact on a company’s bottom line but must not be misread as gains or losses in routine business operations. An exceptional item is also a large number with a substantial impact on the company’s profit or loss, but it is closely related to its day-to-day business.

What gets included in an income statement?

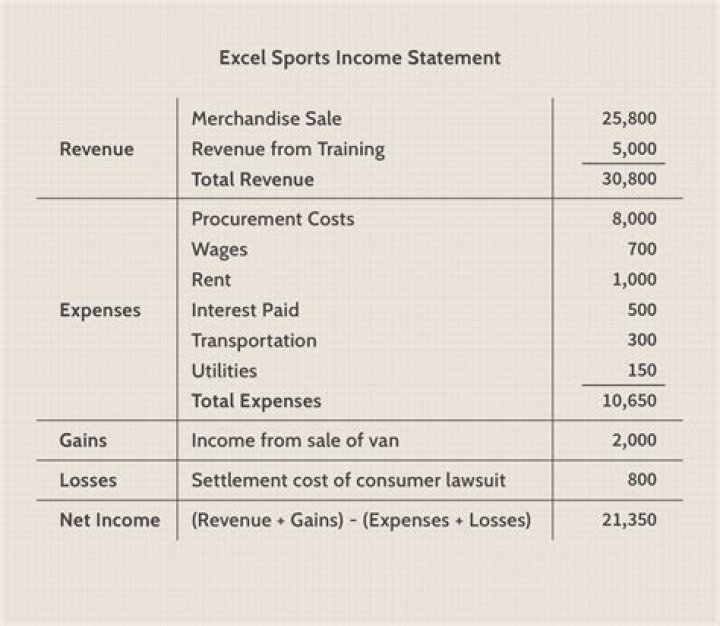

The income statement focuses on four key items—revenue, expenses, gains, and losses. It does not differentiate between cash and non-cash receipts (sales in cash versus sales on credit) or the cash versus non-cash payments/disbursements (purchases in cash versus purchases on credit).

How are extraordinary items reported on an income statement?

The Opinion directed that unusual and nonrecurring items having an earnings or loss effect are extraordinary items (reported in the income statement) or prior period adjustments (reported in the statement of retained earnings). Extraordinary items are reported separately after net income from regular continuing activities.

How are items reported on a corporate income statement?

Accountants determine whether an item is unusual and infrequent in light of the environment in which the company operates.

When does a discontinued operation appear on an income statement?

A discontinued operation occurs when a business sells a segment (usually an unprofitable department or division) to another company or abandons it. When a company discontinues a segment, it shows the relevant information in a special section of the income statement immediately after income from continuing operations and before extraordinary items.

Where does discontinuation of a segment appear on an income statement?

When a company discontinues a segment, it shows the relevant information in a special section of the income statement immediately after income from continuing operations and before extraordinary items. Two items of information appear: