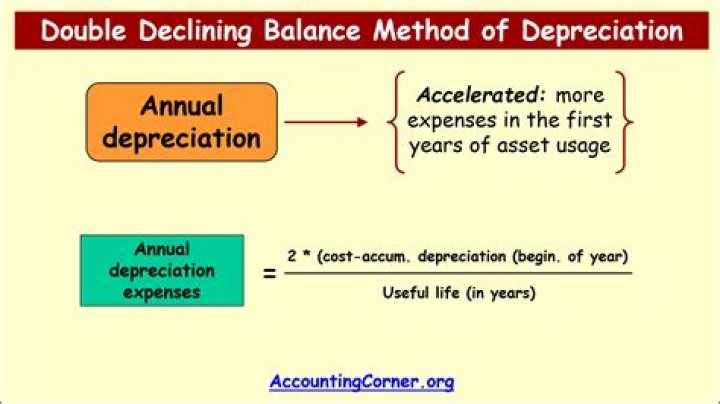

What Is the Double Declining Balance (DDB) Depreciation Method? The double declining balance depreciation method is an accelerated depreciation method that counts as an expense more rapidly (when compared to straight-line depreciation that uses the same amount of depreciation each year over an asset’s useful life).

What is MT depreciation method?

MT – Modified ACRS Using Prescribed IRS Tables Current year depreciable basis for an asset with a method of “MT” is computed as cost minus Section 179 expense, bonus depreciation, Commercial Revitalization/Disaster clean-up & demolition expenses deduction, and ITC basis reduction.

Why would you use accelerated depreciation?

Accelerated depreciation is any depreciation method that allows for the recognition of higher depreciation expenses during the earlier years. Companies may use accelerated depreciation for tax purposes, as these methods result in a deferment of tax liabilities since income is lower in earlier periods.

What is the declining balance method?

The declining balance method is an accelerated depreciation system of recording larger depreciation expenses during the earlier years of an asset’s useful life and recording smaller depreciation expenses during the asset’s later years.

What is the difference between straight line depreciation and double declining balance?

Timing Differences The straight-line method depreciates an asset by an equal amount each accounting period. The declining balance method allocates a greater amount of depreciation in the earlier years of an asset’s life than in the later years.

What is the benefit of accelerated depreciation versus straight-line depreciation?

It is better to take income tax savings earlier in the life of an asset. Straight-line depreciation is easier to calculate and looks better for a company’s financial statements. This is because accelerated depreciation shows less profit in the early years of asset acquisition.

Why is accelerated depreciation better than straight-line?

Accelerated depreciation is unlike the straight-line depreciation method, where the latter spreads the depreciation expenses evenly over the life of the asset. Companies may use accelerated depreciation for tax purposes, as these methods result in a deferment of tax liabilities since income is lower in earlier periods.