Your required minimum distribution is the minimum amount you must withdraw from your account each year. Your withdrawals will be included in your taxable income except for any part that was taxed before (your basis) or that can be received tax-free (such as qualified distributions from designated Roth accounts).

Are required minimum distributions taxable income?

Your RMD is taxed as ordinary income at your personal federal income tax rate. State taxes may also apply.

Where do you put RMD money?

New investments Although your RMD can’t be reinvested back into a tax-advantaged retirement account, you can put money into taxable brokerage accounts and then reinvest your RMD proceeds according to a strategy that fits your needs.

When do you have to take a required RMD?

Withdraw From Your IRALog In Required. When you reach age 70½, you’re required to withdraw a certain amount of money from your retirement accounts each year. That amount is called a required minimum distribution, or RMD.

How are RMDs calculated for a retirement account?

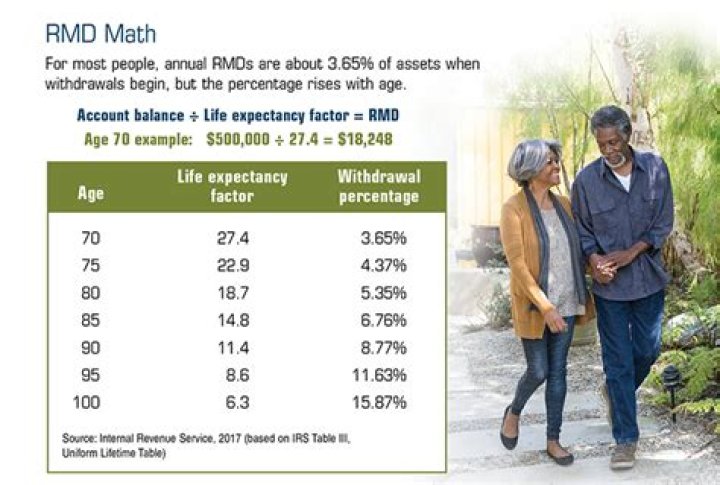

To calculate your RMDs for any given year you need two things: your total retirement account balances as of December 31 of that year, and the age you reach that year. Most retirees will use Table III below to determine what’s called the “distribution period”.

Do you have to pay taxes on RMD distributions?

For most retirement savers, paying taxes on distributions is a necessary evil because they need the money, but affluent retirees with a sizable nest egg may want to hold off if they can find a way to avoid taking them. A big knock against RMDs is the taxes investors have to pay as a result of drawing down some of their retirement savings.

What should I do with my RMD from my IRA?

1. Consider A Charitable Contribution. When you direct your RMD to a charity, it becomes a qualified charitable distribution, or QCD, which is no longer considered taxable income. IRA owners who are at least 70 ½ may transfer as much as $100,000 directly to charity each year, tax-free.