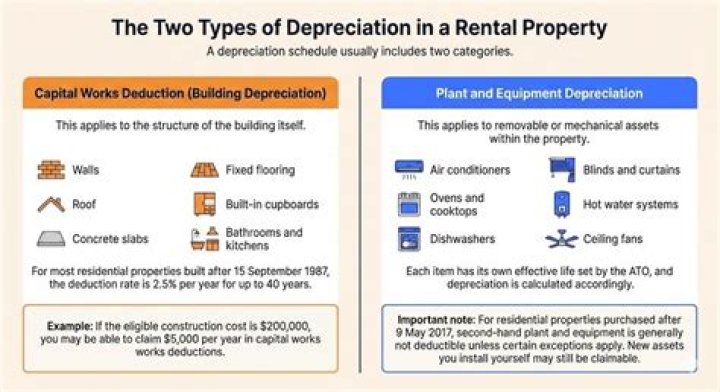

By convention, most U.S. residential rental property is depreciated at a rate of 3.636% each year for 27.5 years. Only the value of buildings can be depreciated; you cannot depreciate land.

Does 27.5 year property qualify for bonus depreciation?

Benefits for Real Estate Investments Buildings are generally depreciated over a 27.5 or 39 year life and bonus depreciation only applies to assets with a recovery period of 20 years or less.

Can I take accelerated depreciation on rental property?

Accelerated Depreciation Those items can be depreciated over shorter time schedules of 5, 7, and 15 years. By creating paper losses from depreciation, we can offset current yield from the property for years. It’s even possible to use any excess against other sources of K-1 passive activity gains.

What are the rules for depreciation on rental property?

There are certain rental property depreciation rules that the IRS expects you to follow. They include using the MACRS that spreads costs and depreciation deductions over 27.5 years for residential properties and 39 years for commercial properties. Keep in mind that we are using the GDS of MACRS and not the ADS.

How is depreciation calculated in a real estate calculator?

Real Estate Property Depreciation. The depreciation of an asset is spread evenly across the life. This calculator is specific for property that is real estate. The key difference from normal straight line depreciation is that a mid month convention is used in calculating depreciation in the first and last years.

When does a property go into service do you get depreciation?

Conventions govern how real property that is put into service in the middle of a year is to be treated from a depreciation perspective. For example, should the property be treated as put into service in the month that it was put into service or the quarter that it was put into service.

How does depreciation recapture affect real estate investors?

Rental property depreciation recapture is the gain that the real estate investor receives from selling the investment property, and it must be reported as income to the IRS. This can hurt an investor because it’s additional income that you have to pay taxes on based on your ordinary tax rate, which can be in addition to capital gains tax.