To close income summary, debit the account for $61 and credit the owner’s capital account for the same amount. In partnerships, a compound entry transfers each partner’s share of net income or loss to their own capital account. In corporations, income summary is closed to the retained earnings account.

What is income Summary In closing entries?

The income summary is a temporary account used to make closing entries. All temporary accounts must be reset to zero at the end of the accounting period. The income summary account then transfers the net balance of all the temporary accounts to retained earnings, which is a permanent account on the balance sheet.

How do you record income summary account?

The income summary entries are the total expenses and total income from your company’s income statement. To calculate the income summary, simply add them together. Then, you transfer the total to the balance sheet and close the account.

What is a closing journal entry?

A closing entry is a journal entry made at the end of the accounting period. It involves shifting data from temporary accounts on the income statement to permanent accounts on the balance sheet. All income statement balances are eventually transferred to retained earnings.

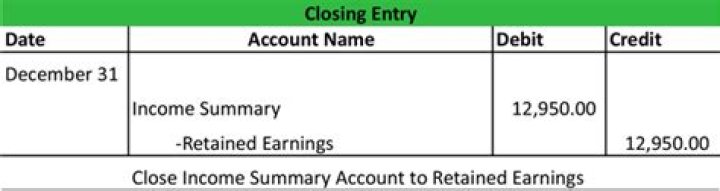

How do you close the income summary account to retained earnings?

Closing Income Summary

- Create a new journal entry.

- Select the Income Summary account and debit/credit it by the Net Income amount noted from the Profit and Loss Report.

- Select the retained earnings account and debit/credit the same amount as the income summary.

- Select Save and Close.

What are the four closing journal entries?

Recording closing entries: There are four closing entries; closing revenues to income summary, closing expenses to income summary, closing income summary to retained earnings, and close dividends to retained earnings.

What type of account is income summary?

Income Summary is a temporary account in which all the closing entries of revenue and expenses accounts are netted at the end of the accounting period, and the resulting balance is considered as profit or loss.

What is income Summary method?

The income summary account is a temporary account into which all income statement revenue and expense accounts are transferred at the end of an accounting period. The net amount transferred into the income summary account equals the net profit or net loss that the business incurred during the period.

Which is closed to the income summary account during the closing process?

Only revenue, expense, and dividend accounts are closed—not asset, liability, Common Stock, or Retained Earnings accounts. The four basic steps in the closing process are: Closing the revenue accounts—transferring the credit balances in the revenue accounts to a clearing account called Income Summary.

How do you write a closing journal entry?

Four Steps in Preparing Closing Entries

- Close all income accounts to Income Summary.

- Close all expense accounts to Income Summary.

- Close Income Summary to the appropriate capital account. Owner’s capital account for sole proprietorship.

- Close withdrawals/distributions to the appropriate capital account.

How do you close a journal entry with income summary?

Closing Entries Using Income Summary 1 Permanent Versus Temporary Accounts. The chart of accounts can be broken down into two categories: permanent and temporary accounts. 2 Updating the Balance in Retained Earnings. Think back to all the journal entries you’ve completed so far. 3 Using Income Summary in Closing Entries.

What is the closing entry for net income?

At the end of the period, the company will need to make the closing entry for net income by transferring all revenues and expenses to the income summary account. Likewise, all revenue accounts and all expenses accounts will be closed by transferring all revenues and expenses to the income summary account.

What are closing entries in accounting?

Closing entries allow a corporation to close temporary accounts, such as revenue and expenses. Closing temporary accounts to the company’s income summary account allows the company to begin the next accounting cycle with a zero balance in the revenue and expense accounts.

How do you write a closing Income Summary for a company?

Closing Income Summary Write the date when the company transfers the income summary balance to the retained earnings account. Draft the day and month when the company closes the income summary account. Debit income summary for the balance contained in the income summary account.