In MACRS straight line, LN calculates the percentage for a year by dividing one depreciation period by the remaining life of the asset, and then applying this amount with the averaging convention to determine the depreciation amount for that year.

How does MACRS depreciation work?

The MACRS depreciation method allows for larger deductions in the early years of an asset’s life, and lower deductions in later years. This contrasts significantly with straight-line depreciation, wherein you claim the same tax deduction each year, until the end of the asset’s usable life.

Why MACRS is used for tax purposes explain the merits and demerits of this method of depreciation?

The MACRS depreciation method allows greater accelerated depreciation over the life of the asset. This means that the business can take larger tax deductions in the initial years and deduct less in later years of the asset’s life. With the straight line or other methods of accelerated cost depreciation.

How might the MACRS system be beneficial for tax purposes for individuals and/or businesses?

MACRS allows for greater accelerated depreciation over longer time periods. This is beneficial since faster acceleration allows individuals and businesses to deduct greater amounts during the first few years of an asset’s life, and relatively less later.

Can you use straight line depreciation for tax purposes?

Although some companies use the straight-line method for tax depreciation, it is not commonly used because it recognizes less depreciation expense in the beginning compared to other methods.

Do you have to use MACRS depreciation?

Most assets acquired after 1986 must be depreciated using MACRS, but other methods may be allowed. Theoretically, the cost of an asset should be deducted over the number of years that the asset will be used, according to the actual drop in value that the asset will suffer each year.

What depreciation method is used for tax purposes?

The straight-line method is the simplest and most commonly used way to calculate depreciation under generally accepted accounting principles. Subtract the salvage value from the asset’s purchase price, then divide that figure by the projected useful life of the asset.

Is Straight line depreciation allowed for tax purposes?

What are the impacts of different depreciation methods on tax?

The larger the depreciation expense, the lower the taxable income, and the lower a company’s tax bill. The smaller the depreciation expense, the higher the taxable income and the higher the tax payments owed.

What is the method of calculating depreciation?

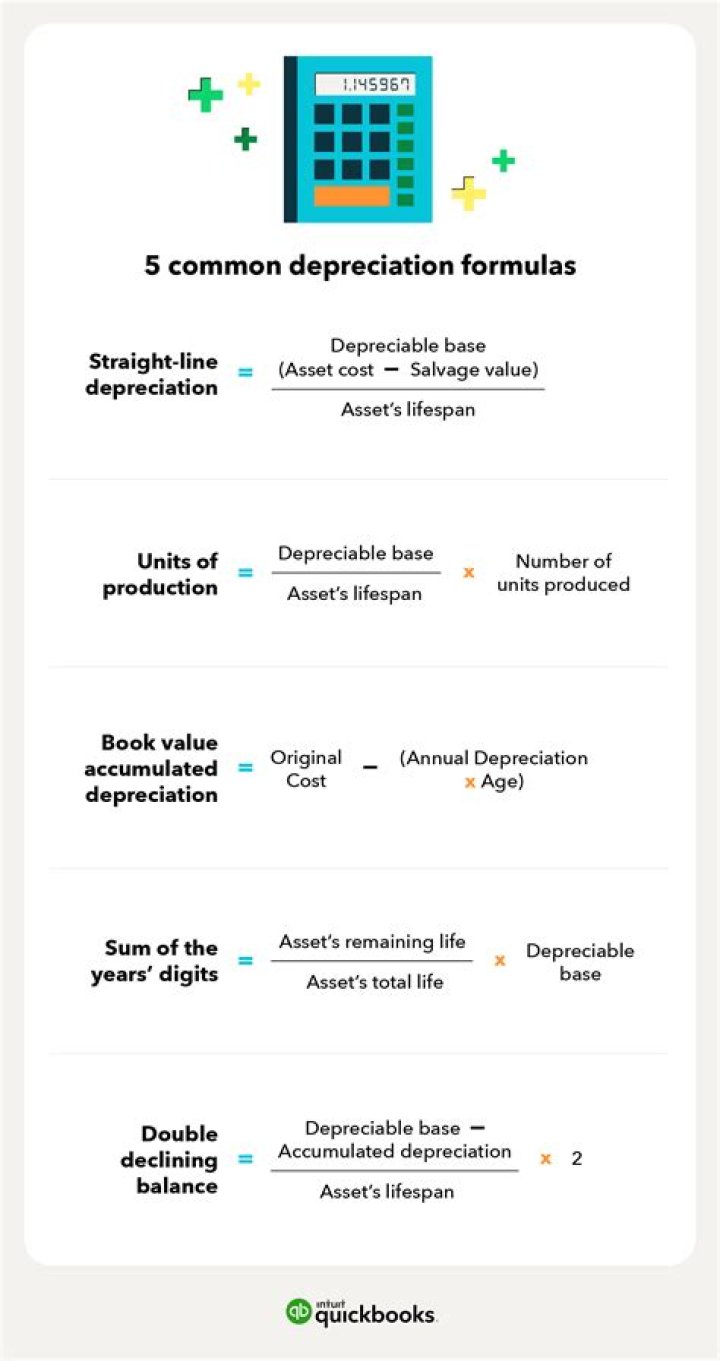

There are four methods for depreciation: straight line, declining balance, sum-of-the-years’ digits, and units of production.

Can I use straight line depreciation for tax purposes?

What is the difference between tax depreciation and accounting depreciation?

In accounting, depreciation is referred to as the cost of a tangible asset. On the other hand, for tax purposes, depreciation is considered as a tax deduction for the recovery of the costs of assets employed in the company’s operations. Thus, depreciation essentially reduces the taxable income.