An advantage of a bare trust is that it is not a reportable entity for taxation and does not need to have its own ABN or TFN. All expenses and deductions claimed for the property are generally included in the fund’s annual return, so the bare trust should not lodge its own, separate return.

Who pays tax on a bare trust?

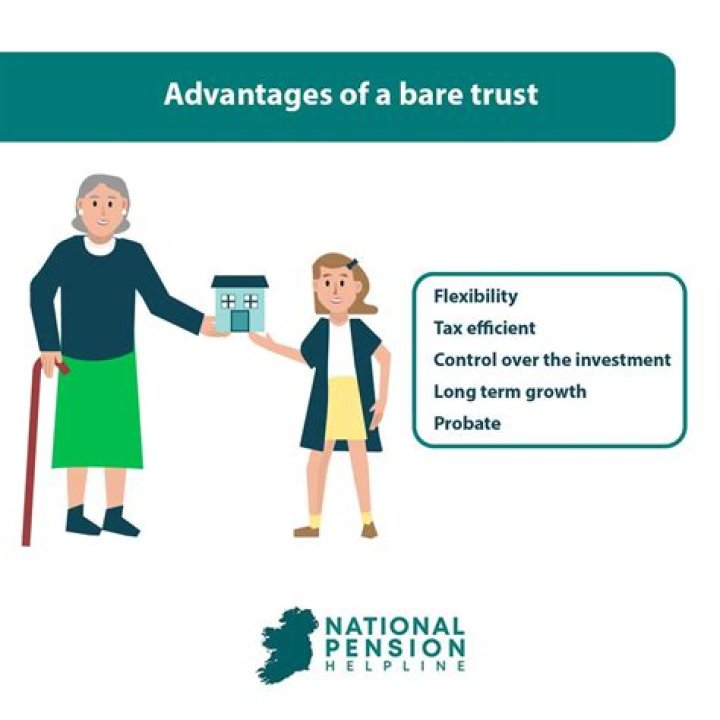

The assets of a bare trust are treated for tax purposes as if the beneficiary holds the trust property in their own name and the beneficiary is liable to Income Tax on income received. The beneficiaries of a bare trust need to account for any Income Tax or Capital Gains Tax on their Self Assessment tax return.

Is there a penalty for filing a trust return late?

Late Filing of Return The law provides a penalty of 5% of the tax due for each month, or part of a month, that the return isn’t filed up to a maximum of 25% of the tax due.

How do you file a tax return for a trust?

Make sure that you tick the Final Return box on the face of the return. And, in case you think the IRS may miss that little box, feel free to also write “Final Return” across the top of the first page. Make sure that the return shows that the trust has reached zero taxable income and zero tax liability.

When to tell HMRC about income from a trust?

You need to tell HMRC about the income on a Self Assessment tax return. If you do not usually send a tax return, you need to register for self-assessment by 5 October following the tax year you had the income. The settlor is responsible for Income Tax on these trusts, even if some of the income is not paid out to them.

When do you have to pay tax on a trust?

If you do not usually send a tax return, you need to register by 5 October following the tax year you had the income. The settlor is responsible for Income Tax on these trusts, even if some of the income is not paid out to them. However, the Income Tax is paid by the trustees as they receive the income.

When do I need to update my trust and estate tax return?

The form and notes have been added for tax year 2020 to 2021. Section for pension payment charges on page TTCG 12 and box T7.30 on page TTCG13 of the Trust and Estate tax calculation guide (2020) have been updated.