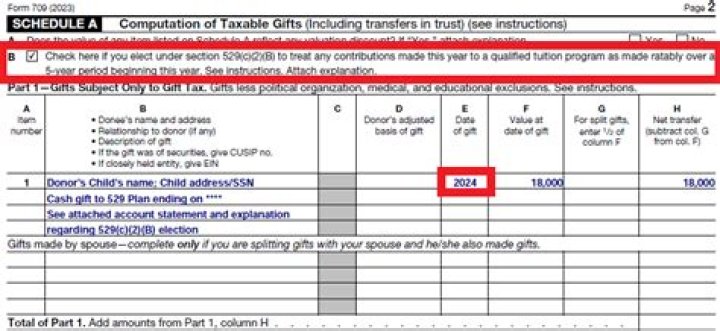

Annual gift tax exclusion One of the many benefits of saving for a child’s future college education with a 529 plan is that contributions are considered gifts for tax purposes. There is no joint gift-tax return, so you and your spouse will each have to file separately.

What happens if you contribute too much to 529?

Saving too much in a 529 plan is an expensive mistake Money is invested and withdrawn tax-free if spent on qualified educational expenses. But if your savings exceed the cost, you may have to pay tax plus a 10% penalty on what’s leftover.

Can both parents contribute to 529 plan?

The short answer is yes — the same child can be the beneficiary of multiple 529 plan accounts. If several people — parents and two sets of grandparents, for instance — want to help fund a child’s education, they can either contribute to a single 529 account or set up separate plan accounts.

How much can each parent contribute to 529?

In either case, parents receive the same treatment as any other person making a contribution: each parent can give up to $15,000 annually to their child’s 529 plan without having to file a gift tax return, for a total of $30,000 per year.

What are the rules for contributions to a 529 plan?

Like contribution limits, minimums vary by plan, so be sure to ask your plan administrator. Here are a few other basic rules that apply to most 529 plans: Only cash contributions are accepted (e.g., checks, money orders, credit card payments). You can’t contribute stocks, bonds, mutual funds, and the like.

What’s the maximum contribution to a vanguard 529 plan?

The Vanguard 529 Plan maximum contribution limit is $500,000. So although you can’t make any additional contributions to your account once you’ve reached that limit, your account can continue to have the potential to grow over time. Will I get penalized if money in my 529 savings plan isn’t used for college?

What are the different types of 529 plans?

There are two main types of 529 plans: prepaid tuition plans, in which the plan holder pays in advance for the beneficiary’s tuition and fees at a specific school, and savings plans, which are tax-advantaged investment vehicles similar to individual retirement accounts (IRAs). 6 How Are 529 Contribution Limits Determined?

Can a 529 plan be used for a non qualified distribution?

If the 529 plan is a custodial 529 plan, distributions from the 529 plan must be used for the benefit of the beneficiary, not the parents. So, a non-qualified distribution can be invested in an annuity for the student, not the parents.