If a business has a reasonable cause for not filing Form 2553 on time, the IRS may approve the S Corp election retroactive to the start of the LLC’s or C Corporation’s tax year. The business owner must explain on Form 2553 why the filing was submitted late.

How late can you file S corp election?

When To Make the Election Complete and file Form 2553: No more than 2 months and 15 days after the beginning of the tax year the election is to take effect, or. At any time during the tax year preceding the tax year it is to take effect.

When do I need to file a late 2553?

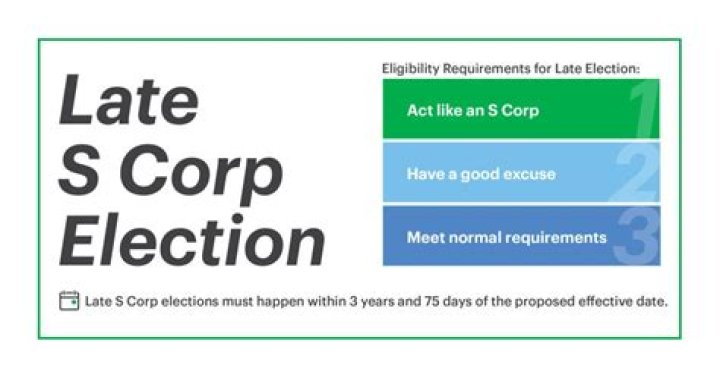

A late election to be an S corporation and a late entity classification election for the same entity may be available if the entity can show that the failure to file Form 2553 on time was due to reasonable cause. Relief must be requested within 3 years and 75 days of the effective date entered on line E of Form 2553.

When to file Form 2553 for single member LLC?

Form 2553 is used to tell the IRS that you want a corporation (or entity eligible to be taxed as a corporation, such as a single member LLC) to be taxed as a S-Corp. It is due: No more than 2 months and 15 days after the beginning of the tax year the election is to take effect,

Can a corporation fail to qualify on Line E of Form 2553?

The corporation fails to qualify as an S corporation (see Who May Elect, earlier) on the effective date entered on line E of Form 2553 solely because Form 2553 wasn’t filed by the due date (see When To Make the Election, earlier);

How to request relief from late filing for reasonable cause?

To request relief from a late filing for reasonable cause, complete the narrative section at the bottom of Page 1, explaining why you are filing late (you can use the text from page 4 of Form 2553). 5. Mail or fax the Signed Form 2553 to the IRS. Next, wait for the IRS’s decision, and enjoy your new S-Corp status.