The legislation allowed people to take distributions of up to $100,000 from their 401(k) accounts or IRAs without having to pay the normal 10% penalty in 2020, even if they were younger than age 59 1/2. The law allows you to stretch the taxes due on a 2020 retirement account withdrawal over three years.

Why am I getting taxed twice on 401k withdrawal?

But, no, you don’t pay taxes twice on 401(k) withdrawals. With the 20% withholding on your distribution, you’re essentially paying part of your taxes upfront. Depending on your tax situation, the amount withheld might not be enough to cover your full tax liability.

What is the tax penalty for taking money out of a 401k?

Assume the 401 (k) in the example above is a traditional account and your income tax rate for the year you withdraw funds is 20%. In this case, your withdrawal is subject to the vesting reduction, income tax, and the additional 10% penalty tax. The total tax impact become 30% of $16,250, or $4,875.

What happens if I withdraw money from my 401k early?

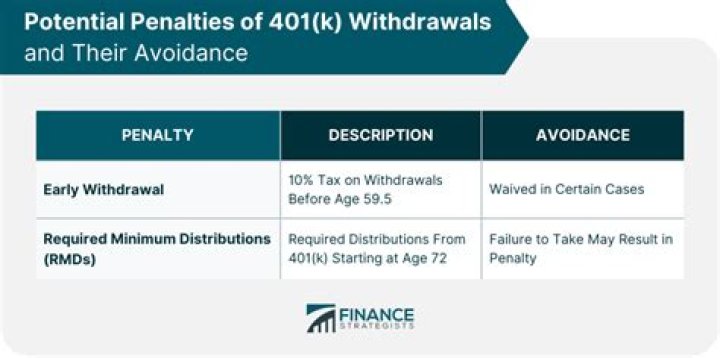

Participants in a traditional or Roth 401 (k) plan are not allowed to withdraw their funds until they reach age 59½. If you withdraw funds early from a 401 (k) you will be charged a 10% penalty tax, plus your tax rate on the amount you withdraw. In short, if you withdraw retirement funds early, the money will be treated as income.

How old do you have to be to withdraw from a 401k penalty free?

The IRS allows penalty-free withdrawals from retirement accounts after age 59 1/2 and requires withdrawals after age 70 1/2 (these are called Required Minimum Distributions [RMDs]). There are some exceptions to these rules for 401ks and other ‘Qualified Plans.’

When do you have to pay taxes on a 401k distribution?

Generally, if you take a distribution from an IRA or 401k before age 59 ½, you will likely owe both federal income tax (taxed at your marginal tax rate) and a 10% penalty on the amount that you withdraw, in addition to any relevant state income tax. That tends to add up.