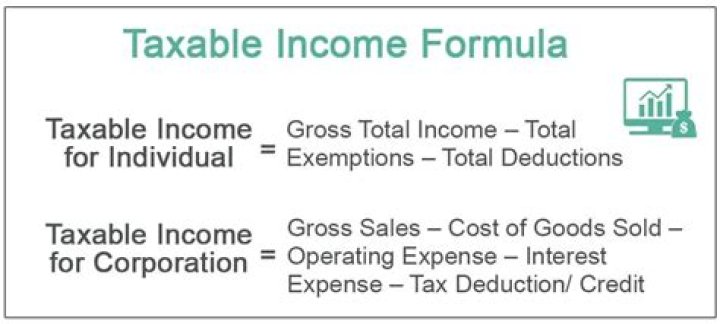

Taxable Income. Book income is used by companies to report their income and expenses to shareholders. Taxable income is used by businesses to report earnings and tax liability to tax authorities.

What is book income vs tax income?

Book income describes a company’s financial income before taxes. It is the amount a corporation reports to its investors or shareholders and gives an idea of how well a company performed during a certain period of time. Tax income, on the other hand, is the amount of taxable income a company reports on its return.

How do you reconcile income from book tax?

Tax Return Reconciliation The schedules start with accounting income, increase it with expenses that aren’t tax-deductible and income that is taxable but not yet reported on the books, then decreases it for book income that’s not taxed and tax deductions that exceed book expenses.

How can I reduce my interest income on my taxes?

Is there any way to avoid taxes on interest income?

- Keep assets in tax-exempt accounts, such as a Roth IRA or a Roth 401(k).

- Keep assets in education-oriented accounts, like 529 plans and Coverdell education savings accounts.

Why are there differences between taxable and financial income?

One reason financial income can be different from taxable income is that the IRS does not accept certain income deductions. You would show such an expense on your business records, but could not claim it on your tax return. This would give you a different figure for net taxable income than for net financial income.

What is meant by book profit in income tax?

Book profits refer to the profit earned by the business entity from its operations and activities and is calculated by deducting all the business expenses incurred within a financial year from all the sales revenue and other income generated from the selling of goods & services within that same financial year.

What is the difference between book and tax depreciation?

Fixed Assets The main difference in book and tax depreciation is the timing of the depreciation, but the overall depreciation expense is the same throughout the life of an asset. The legally mandated tax depreciation method is the Modified Accelerated Cost Recovery System (MACRS).

What is non taxable interest income?

Tax-exempt interest is interest income that is not subject to federal income tax. The most common sources of tax-exempt interest come from municipal bonds or income-producing assets inside of Roth retirement accounts.

Is interest income included in gross income?

Gross income refers to the total income earned by an individual on a paycheck before taxes and other deductions. It comprises all incomes received by an individual from all sources – including wages, rental income, interest income, and dividends.

What is TDS payable?

TDS stands for tax deducted at source. As per the Income Tax Act, any company or person making a payment is required to deduct tax at the source if the payment exceeds certain threshold limits. It is the deductor’s responsibility to deduct TDS before making the payment and deposit the same with the government.

Is income tax an expense?

The income tax expense is reported as a line item in the corporate income statement, while any liability for unpaid income taxes is reported in the income tax payable line item on the balance sheet.

Is depreciation a DTA or DTL?

DTL – Common example of DTL would be depreciation. When the depreciation rate as per the Income tax act is higher than the depreciation rate as per the Companies act (generally in the initial years), entity will end up paying less tax for the current period.

Is taxable income the same as interest income?

No matter the source, most interest earned by your savings and investments counts as taxable income. It’s taxed at the same rate as ordinary income — based on your regular tax bracket for the year.

What are book to tax differences?

Here is a list of the common book-to-tax differences we see so that you can understand the differences between your book and taxable income.

- Depreciation and amortization.

- Allowance for doubtful accounts.

- Inventory reserves for slow-moving, excess or obsolete inventory.

- Accrued accounts.

- Travel and entertainment.

How is book tax expense calculated?

Tax expenses are calculated by multiplying the appropriate tax rate of an individual or business by the income received or generated before taxes, after factoring in such variables as non-deductible items, tax assets, and tax liabilities.

What is the exemption limit for interest income?

₹10,000

If you are filing your tax return, don’t forget to claim these deductions and exemptions to save tax on interest income. Most of you would know that you can claim a deduction of up to ₹10,000 on the interest earned on a savings bank account under Section 80TTA of the Income Tax Act.

What does book to tax mean?

A book-to-tax reconciliation is the act of reconciling the net income on the books to the income reported on the tax return by adding and subtracting the non-tax items. The tax exempt income is simply subtracted from book income in the book-to-tax reconciliation.

The major difference between book depreciation and tax depreciation is timing. It includes the timing of when the price of an asset will reflect as depreciation expenditure on the company’s financial statement against depreciation expenditure on the organisation’s income tax return.

What are the differences between book and tax?

Permanent book-tax differences arise from items or deductions for either book or tax purposes, but not both. These items do not reverse over time, thus the total amount of income or deductions for such items is different for book and tax purposes.

Which is an unfavorable permanent book tax difference?

As a result, federal income tax expense constitutes a permanent and unfavorable book-tax difference that must be added back to book income to determine taxable income. Another very common permanent book-tax difference is the interest income from municipal bonds.

Are there any tax deductions for book income?

For tax purposes, a company can only deduct 50%of meals and 0% of entertainment expenses. Municipal bond interest – This is considered net income for book accounting, but it is not included in taxable income.

What is the difference between interest income and interest expense?

The main difference between interest income and interest expense is outlined below: 1 Interest income is money earned by an individual or company for lending their funds, either by putting them into a… 2 Interest expense, on the other hand, is the opposite of interest income. It is the cost of borrowing money from… More …