Schedule K-1 allows your beneficiary to separate his or her income distribution into all the sorts of income received by the trust or estate. Because it is an attachment to Form 1041, you must distribute a copy of it to the income beneficiaries no later than the due date for Form 1041, as extended.

Who is likely to receive a K-1 form?

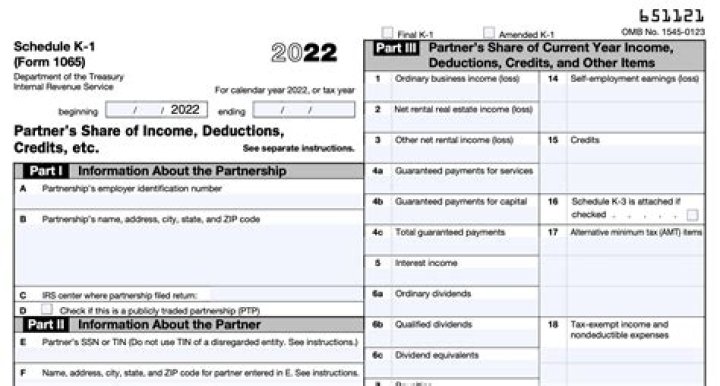

A K-1 is a tax form distributed by many partnerships, S-Corps, estates, and trusts. If you are a general or limited partner of a partnership, a shareholder in an S-Corp, or the beneficiary of an estate or trust, you’re likely to receive a K-1. You: But what is it? A K-1 is just like a W-2 or other tax form.

Do you have to attach a copy of your K-1 to a 1041?

You must furnish a copy of each K-1 to the appropriate beneficiary, and attach all copies to Form 1041 when you file the return with the Internal Revenue Service. Since the trust and estate must report all income, deductions are available for amounts that must be distributed to beneficiaries.

When is the due date for a K-1 tax return?

The due date for most partnership tax returns is March 15. Consequently, K-1s are often received much later than other tax forms. Furthermore, like individuals, partnerships can request extensions of time to file, often until September 15.

Can a trust and estate report income on Form 1041?

Trust and estate deductions. Since the trust and estate must report all income, deductions are available for amounts that must be distributed to beneficiaries. Form 1041 allows for an “income distribution deduction” that includes the total income reported on all beneficiary K-1s.

What do you need to know about the 1041 form?

Since the trust and estate must report all income, deductions are available for amounts that must be distributed to beneficiaries. Form 1041 allows for an “income distribution deduction” that includes the total income reported on all beneficiary K-1s.