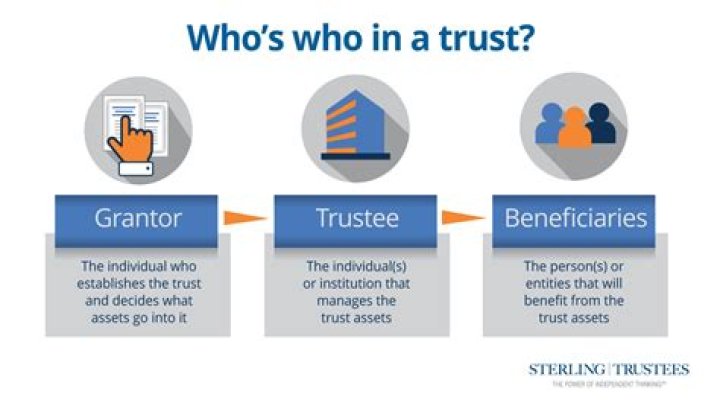

A beneficiary of trust is the individual or group of individuals for whom a trust is created. The trust creator or grantor designates beneficiaries and a trustee, who has a fiduciary duty to manage trust assets in the best interests of beneficiaries as outlined in the trust agreement.

Is grantor and beneficiary same person?

Grantor is the legal term for a person who creates a trust, and beneficiaries are people named by the grantor to benefit from the trust by receiving the trust’s property. The legal terms “grantor,” “settlor,” and “creator” have the same meaning and can be used interchangeably.

What is the difference between a settlor and a grantor?

Settlor and grantor are two different names for the person who creates a trust. The settlor and grantor are both terms that refer to the person who creates a trust. As part of an estate plan, the settlor/grantor transfers assets into a trust for the future use of their beneficiaries.

Who are the beneficiaries of a land trust?

The grantor is the landowner, and, in most cases, the beneficiary of a land trust is also the landowner. The trustee is the person or firm that takes ownership — at least on paper — of the property. A land trust can involve joint owners and multiple beneficiaries.

Who are the parties in a land trust?

A land trust is a legal entity that involves a grantor, a trustee, and a beneficiary. These parties are the same as those in any other trust. The grantor is the landowner, and, in most cases, the beneficiary of a land trust is also the landowner. The trustee is the person or firm that takes ownership — at least on paper — of the property.

How does a beneficiary grantor trust work?

Because the child has given up a right to remove available funds, the $5,000 stays in the trust, where it is held and managed for the child’s benefit. The child, who is also the trustee, gets to decide not only how to invest the $5,000 but how to make distributions under the standard of health, education, maintenance and support.

When was the grantor trust rule first created?

The grantor trust rules were first developed in the late 1960s in order to thwart taxpayers’ use of trusts to shift income into lower tax brackets.