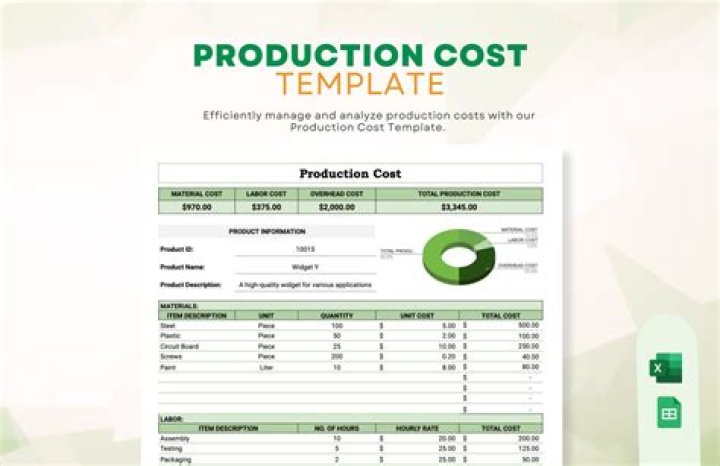

The cost of production report (CPR) is a document used in process costing system that summarizes the information about the flow of units and costs through the work in process account of a processing department. It is equal to the job cost sheet prepared in a job order costing system.

What is the treatment of transferred in goods in process costing system?

Transferred-in goods are treated as if they are a separate material category that is added at the beginning of the process for the equivalent units and unit cost computations. The transferred-in units have 100% of the work and costs of the prior process.

What is a production cost report used for?

The production cost report. summarizes the production and cost activity within a department for a reporting period. It is simply a formal summary of the four steps performed to assign costs to units transferred out and units in ending work-in-process (WIP) inventory.

What is the cost of production report?

A production cost report details the total cost, including raw materials and operating costs, of producing a product. Production cost reports (PCRs) are also sometimes called cost of production reports, product cost reports or process cost summaries.

What are transferred in costs in process costing system?

Transferred-in cost is the cost that a product accumulates during its tenure in upstream work centers. Thus, it is the accumulated cost of a product when it first arrives in a downstream work center. This concept is used in a process costing system.

How does the production cost report process work?

How are cost of production reports used for controlling?

The cost of production report provides information for controlling and improving operations. Most cost of production reports include the detailed manufacturing costs incurred for completing production during the period. Analyzing trends in each of these costs over time can provide insights about process performance.

What is the importance of production report?

Answer: It provides information regarding input units, opening inventory balance, completed units, transferred units, equivalent units, cost per equivalent units, cost of production of units produced and units sold out, and cost of ending inventory.