When preparing a statement of cash flows using the indirect method, depreciation expense is added to net income to arrive at net cash flows from operating activities.

How do you calculate indirect cash flow?

Under the indirect method, cash flow from operating activities is calculated by first taking the net income from a company’s income statement. Because a company’s income statement is prepared on an accrual basis, revenue is only recognized when it is earned and not when it is received.

What is the indirect method in accounting?

The indirect method presents the statement of cash flows beginning with net income or loss, with subsequent additions to or deductions from that amount for non-cash revenue and expense items, resulting in cash flow from operating activities.

What is indirect method formula?

With the indirect method, cash flow is calculated by taking the value of the net income (i.e. net profit) at the end of the reporting period. The next stage is to add or subtract the changes in the cash value of specific categories that relate to operating activities.

What is the indirect accounting method?

When preparing a statement of cash flows using the indirect method which of the following is correct?

When preparing a statement of cash flows using the indirect method, which of the following is correct? Proceeds from the sale of equipment should be added to net income in the operating activities section. A loss on the sale of land should be added to net income in the operating activities section.

How do you prepare a cash flow statement in accounting?

Cash flow is calculated by making certain adjustments to net income by adding or subtracting differences in revenue, expenses, and credit transactions (appearing on the balance sheet and income statement) resulting from transactions that occur from one period to the next.

How is the change in cash classified on the statement of cash flows?

Question: How is the change in cash classified on the statement of cash flows? It is found in the financing activities section of the statement. It is the sum of the investing, operating, and financing activities sections. It is found in the operating activities section of the statement.

How to prepare Statement of cash flows by indirect method?

Preparing the operating section of statement of cash flows by the indirect method starts with net income from the income statement and adjusts for items that affect cash flows differently than they affect net income. Multiple levels of adjustments are required to reconcile accrual-based net income to cash flows from operating activities.

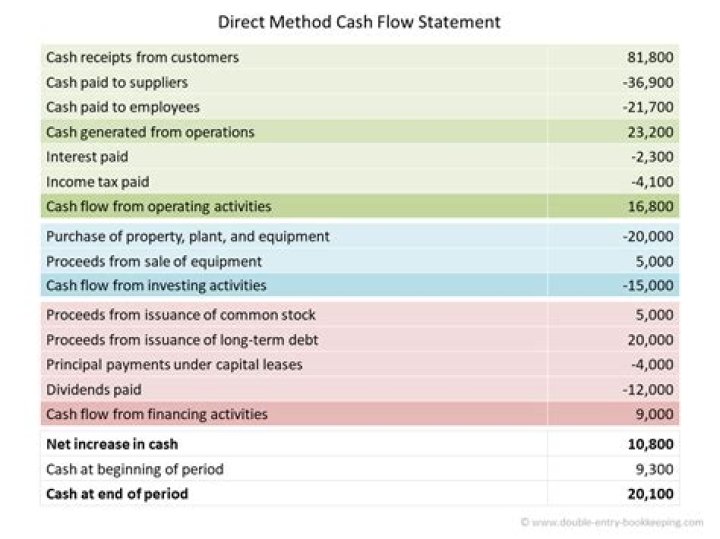

How does direct method work on income statement?

The direct method converts each item on the income statement to a cash basis. For instance, assume that sales are stated at $100,000 on an accrual basis. If accounts receivable increased by $5,000, cash collections from customers would be $95,000, calculated as $100,000 – $5,000.

What are the advantages of the indirect method?

The principle advantage of indirect method is that it focus on the differences between net income and net cash flow from operating activities. That is, it provides a useful link between the statement of cash flows and the income statement and balance sheet.

Why do I need to Subtract income from cash flow statement?

Thus, a net increase in an asset account actually decreased cash, so we need to subtract this increase from the net income. The opposite is true about decreases. If an asset account decreases, we will need to add this amount back into the income. Here’s a general rule of thumb when preparing an indirect cash flow statement: