Powers that Make a Trust a Grantor Trust

- a reversionary interest in either the corpus or the income of the trust.

- if the beneficial enjoyment of the corpus or the income from the trust is subject to a power of disposition by the grantor without the approval or consent of any adverse party.

Can a grantor trust have self employment income?

But, a trust that is treated as a grantor trust under the provisions of I.R.C. §§671-679 is treated as owned directly by the grantor. That’s because the grantor retains the control to direct the trust income or assets. Consequently, trust taxation does not apply, and self-employment tax savings will not be achieved.

Who controls a grantor trust?

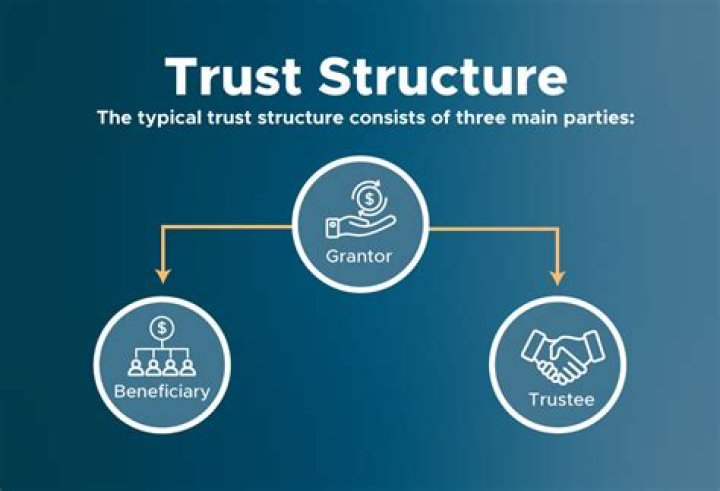

Understanding Grantor Trust Rules However, a grantor trust is any trust in which the grantor or owner retains the power to control or direct income or assets within the trust. 1 In other words, the grantor trust rules allow a grantor to control the assets and investments in the trust.

Does an irrevocable grantor trust need to file a tax return?

If an irrevocable trust has its own tax ID number, then the IRS requires the trust to file its own income tax return, which is IRS form 1041. During the lifetime of the grantor, any interest, dividends, or realized gains on the assets of the trust are taxable on the grantor’s 1040 individual income tax return.

What makes a trust a grantor trust for tax purposes?

Powers that Make a Trust a Grantor Trust. The powers listed below are examples of powers that, if retained by the grantor, should cause a trust to be treated as a Grantor Trust for income tax purposes: a reversionary interest in either the corpus or the income of the trust.

When was the grantor trust rule first created?

The grantor trust rules were first developed in the late 1960s in order to thwart taxpayers’ use of trusts to shift income into lower tax brackets.

Are there any exceptions to grantor trust rules?

The IRS defines eight exceptions to avoid triggering the grantor trust status. For example, if the trust has only a single beneficiary who is paid the principal and income from the trust. Or, if the trust has multiple beneficiaries who receive the principal and income from the trust in accordance with their share holding in the trust.

What does Form 1041 do for grantor trust?

The Form 1041 would have a statement attached to it, and that statement would say all items of the income deduction and credit are being reported on the grantor’s personal return. So, we had a short Form 1041 that simply deflected the IRS over to the grantor’s own personal tax return.