$13,500

2021 SIMPLE IRA Contribution Limits For 2021, the annual contribution limit for SIMPLE IRAs is $13,500, the same amount as the year before. Workers age 50 or older can make additional catch-up contributions of $3,000, for a total of $16,500.

What types of contributions can be made into a SIMPLE IRA?

What types of contributions may be made to a SIMPLE IRA plan?

- matching contribution or.

- nonelective contribution.

How are SIMPLE IRA contributions reported?

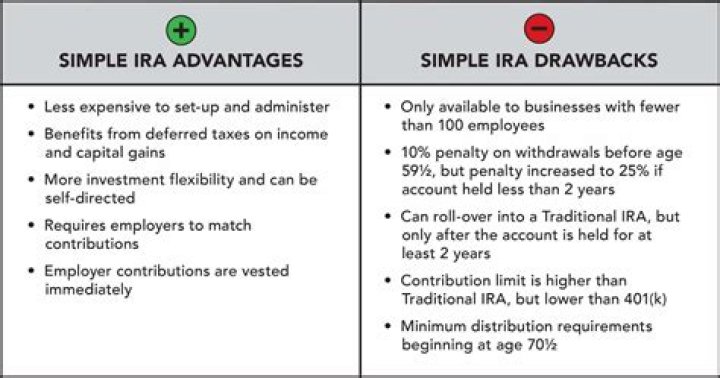

Simple IRA W-2 Reporting Requirements Most small businesses with 100 or fewer employees can set up a SIMPLE IRA. Employee participants report their contributions for the year on Form 1040, Schedule 1, Line 28.

How do I deduct my SIMPLE IRA contributions?

Employee contributions to a SIMPLE IRA plan are not deducted by participants from their income on their Form 1040. If you participated in a SIMPLE IRA plan through your employer, the amount contributed into the plan is already excluded from your Gross Income (Box 1 of W2) for Federal Withholding purposes.

How much does an employer have to contribute to a SIMPLE IRA?

The employer must either match the contributions employees make to their plan, up to 3% of salary. Or the employer can make contributions for employees of a flat 2% of salary, whether or not the employee chooses to participate in the plan.

Is there such a thing as a SIMPLE IRA?

SIMPLE IRA Plan. A SIMPLE IRA plan (Savings Incentive Match PLan for Employees) allows employees and employers to contribute to traditional IRAs set up for employees.

Can a sole proprietor contribute to a SIMPLE IRA?

Businesses, including sole proprietors, with less than 100 employees can set one up. There are two ways contributions are made to a SIMPLE IRA—employers can either match employee contributions or make contributions on their behalf.

What are the deadlines for SIMPLE IRA contributions?

Deadlines for SIMPLE IRA contributions vary by type of contribution and whether the employer or employee is making it. Employers can either match employee contributions or contribute on their behalf. Contributions that are not made on time may incur fees or necessitate filing an amended tax return.