The minimum selling price of the convertible bond is the highest value of the price of a straight bond and the conversion value of the convertible bond. First, we need to find the straight bond value by discounting the semiannual coupon payments and maturity value at 9%.

What is Floor value of convertible bond?

The floor value of the convertible bond is the lowest value to which the bond can drop and the point at which the conversion option becomes worthless. It’s important to know how to calculate this value so that you can sell or convert the bonds while they still retain value.

How do you price a convertible bond?

The conversion price of the convertible security is the price of the bond divided by the conversion ratio. If the bonds par value is $1000, the conversion price is calculated by dividing $1000 by 5, or $200. If the conversion ratio is 10, the conversion price drops to $100.

How do you calculate the minimum value of a convertible bond?

Bond floor refers to the minimum value a bond (usually a convertible bond) should trade for and is calculated using the discounted value of its coupons plus redemption value.

What is the minimum value of the bond?

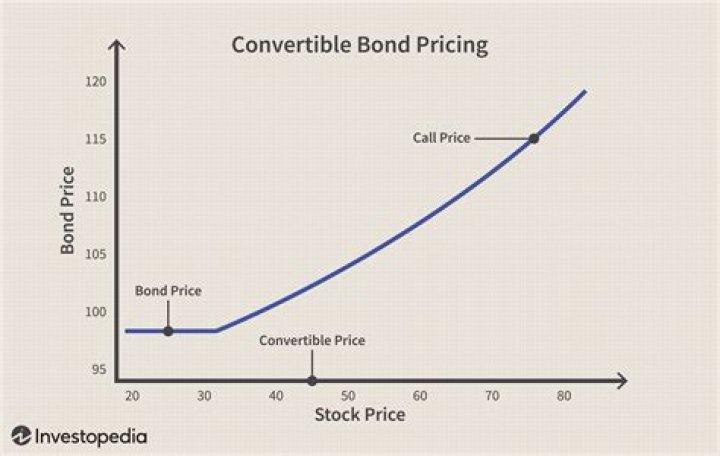

The minimum value of a convertible bond is the “investment value” of its bond component, which is the present value of future coupon payments and principal repayment from the bond. Because of this fact, a convertible bond should be worth at least as much as the value of its underlying shares.

How do you find the minimum value of a convertible bond?

What is a conversion ratio?

The conversion ratio is the number of common shares received at the time of conversion for each convertible security. The higher the ratio, the higher the number of common shares exchanged per convertible security.

What is convexity risk?

Convexity is a risk-management tool, used to measure and manage a portfolio’s exposure to market risk. Convexity demonstrates how the duration of a bond changes as the interest rate changes. If a bond’s duration increases as yields increase, the bond is said to have negative convexity.

When should you convert a convertible bond?

Forced conversion usually occurs when the price of the stock is higher than the amount it would be if the bond were redeemed. Alternatively, it may also occur at the bond’s call date. A reversible convertible bond allows the company to convert it to shares or keep it as a fixed income investment until maturity.

What is the value to the issuer on the conversion feature of convertible debt?

Convertible bonds share qualities of both common stock and bonds. Parity requires values to rise congruently. For example, if your $1,000 bond converts into 50 shares, each share of stock is valued at $20. If stock prices rise to $25 per share, your bond would be valued at $1,250.

What is a good feed conversion ratio?

A FCR (kg feed dry matter intake per kg live mass gain) for lambs is often in the range of about 4 to 5 on high-concentrate rations, 5 to 6 on some forages of good quality, and more than 6 on feeds of lesser quality.

To find the bond floor, one must calculate the present value (PV) of the coupon and principal payments discounted at the straight bond interest rate. So, even if the company’s stock price falls, the convertible bond should trade for a minimum of $884.18.

What is the floor value of a convertible bond?

How are convertible bonds priced?

To accomplish convertible bond valuations, investors may rely on the following formula: Value of convertible bond = independent value of straight bond + independent value of conversion option.

What is parity in convertible bonds?

A convertible bond offers the opportunity to convert into a fixed number of shares of common stock at a specific price per share. Parity price is the market price of the convertible security divided by the conversion ratio (the number of common stock shares received upon conversion).

How do you calculate cost of convertible debt?

Why are convertible bonds cheaper?

If the share price performs strongly and the bonds do end up converting, the stock price still needs to go quite a bit higher than the conversion price before the all-in cost exceeds that of non-convertible debt. However, if the stock has a modest positive performance, the convertible will be cheapest.

What’s the floor price for a convertible bond?

So, even if the company’s stock price falls, the convertible bond should trade for a minimum of $884.18. Like the value of a regular, non-convertible bond, a convertible bond’s floor value fluctuates with market interest rates and various other factors.

Which is an example of a bond floor?

In other words, the bond floor is the value at which the convertible option becomes worthless because the underlying stock price has fallen substantially below the conversion value. For example, assume a convertible bond with a $1,000 par value has a coupon rate of 3.5% to be paid annually. The bond matures in 10 years.

How is the yield of a convertible bond determined?

Identify the yield of the bond. Convertible bond issuers attach a coupon or interest payment to each bond issue. This provides incentive for investors to purchase the debt as they will receive a scheduled interest payment over the life of the bond. Investors refer to this interest payment as the bond yield.

Can a convertible bond be converted to common stock?

Convertible bonds are a hybrid debt instrument issued by a corporation that can be converted to common stock at the discretion of the bondholder or the corporation once certain price thresholds are achieved.