To calculate the forward rate, multiply the spot rate by the ratio of interest rates and adjust for the time until expiration. So, the forward rate is equal to the spot rate x (1 + domestic interest rate) / (1 + foreign interest rate).

How do you interpret forward rates?

The forward exchange rates are quoted in terms of points. For example, let’s say the current EUR/USD exchange rate is 1.2823. The forward quote for a 90-day forward exchange rate is +16 points. This 16 points will be interpreted as 16*1/10,000 = 0.0016 above the spot rate.

How is FRA rate calculated?

Formula and Calculation for a Forward Rate Agreement Calculate the difference between the forward rate and the floating rate or reference rate. Multiply the rate differential by the notional amount of the contract and by the number of days in the contract. Divide the result by 360 (days).

What is forward rate differential?

The percentage difference between the spot price and the forward price of an asset. The forward differential is expressed in annualized terms, and may help the investor determine the general price trend of an asset.

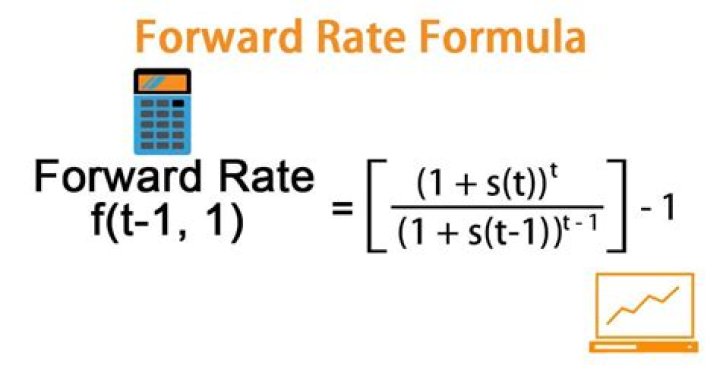

What is the one year forward rate?

A projection of future interest rates calculated from either spot rates or the yield curve. For example, suppose the one-year government bond was yielding 2% and the two-year bond was yielding 4%. The one year forward rate represents the one-year interest rate one year from now.

What is forward discount?

A forward discount is a term that denotes a condition in which the forward or expected future price for a currency is less than the spot price. It is an indication by the market that the current domestic exchange rate is going to decline against another currency.

What is a forward interest rate?

A forward rate is an interest rate applicable to a financial transaction that will take place in the future. The term may also refer to the rate fixed for a future financial obligation, such as the interest rate on a loan payment.

How do you read a forward curve?

The forward curve is static in nature and represents the relationship between the price of a forward contract and the time to maturity of that forward contract at a specific point of time. When the Spot Rave is upward sloping, the forward curve will be above it, and the par curve will be below it.

What is spot rate and forward rate?

A spot rate is used by buyers and sellers looking to make an immediate purchase or sale, while a forward rate is considered to be the market’s expectations for future prices.

What is the two year forward rate starting in one year?

The spot rate for two years, S1 = 7.5% The spot rate for one year, S2 = 6.5% No. years for 2nd bonds, n1 = 2 years….Courses.

| 19th/20th September 2020 | Saturday – Sunday | 9 am IST to 5 pm IST |

|---|---|---|

| 26th/27th September 2020 | Saturday – Sunday | 9 am IST to 5 pm IST |

What is forward premium or forward discount?

Forward premium is when the forward exchange rate is higher than the spot exchange rate. Forward discount is the opposite of forward premium, it when the forward exchange rate is lower than the spot exchange rate. Forward premium or discount is normally expressed as annualized percentage of the difference.

What would happen with a 100% with forward?

What would happen with a 100% hedge with forwards? If AIFS were to hedge against currency risk using 100% forward contracts, their position would be fully covered if they can accurately predict the amount and timing of the payments.

What is a forward rate curve?

The forward curve can be used as a baseline projection of future interest rates to support investment analysis. The forward curve is used to establish the mid-market swap rate as it projects the expected future floating-rate cash flows used to calculate the fixed rate (more info on interest rate swaps).

What do forward curves tell us?

Simply put, a forward curve is a snapshot representation of what a commodity is currently worth today based on a possible buy or sell in the future. Using a forward curve, I can tell you what the price of WTI crude futures is currently for barrels that would change hands in 2024.

For example, suppose the one-year government bond was yielding 2% and the two-year bond was yielding 4%. The one year forward rate represents the one-year interest rate one year from now. You would solve the formula (1.04)^2=(1.02)(1+F).

What is the forward rate market?

The forward exchange market is a market for contracts that ensure the future delivery of a foreign currency at a specified exchange rate. The price of a forward contract is known as the forward rate.

What is the forward rate used for?

Forward rate is the theoretical yield on a bond that will occur in the future (in most cases, several months or years from the time of the calculation). Yield is a term referring to the return on the bond buyer’s investment. Generally, forward rate is used when discussing the purchase of T-bills, or Treasury bills.

What is forward rate curve?

An interest rate forward curve for a market index is, at a discrete moment in time, a graphical representation of the market clearing forward rates for that index. LIBOR forward curves are derived from observable data including Eurodollar deposits, Eurodollar futures, and LIBOR swap rates1.

How forward rates are quoted?

Forward points are often quoted in numbers, such as +13.2 or minus -270.68. These represent 1/10,000, so +13.2 means 0.00132 when added to a currency spot price. This is because the forward points compensate for the difference in interest rates between the two currencies.

What is difference between spot rate and forward rate?

In commodities markets, the spot rate is the price for a product that will be traded immediately, or “on the spot.” A forward rate is a contracted price for a transaction that will be completed at an agreed upon date in the future.

How do you convert forward points to forward rates?

Using Forward Points to Compute the Forward Rate It is written as 170/10,000 and is added to the spot price to estimate the forward rate. The fraction 170/10,000 equates to 0.017 units. Hence, the forward rate will be computed by adding the 0.017 units to the current spot rate.