There is one key difference between a W-2 form and a 1099. A Form 1099 is issued to an independent contractor to report their income to the IRS. They pay their taxes since they are self-employed. A Form W-2 is given to an employee to report their income and payroll taxes withheld.

Is it better to be paid 1099 or W-2?

1099 contractors have a lot more freedom than their W2 peers, and thanks to a 2017 corporate tax bill, they are allowed significant additional tax deductions from what is called a 20% pass-through deduction. However, they often receive fewer benefits and have far more tenuous employment status with their organization.

Does 1099 get a W-2?

If you’re an independent contractor, you get a 1099 form. If you’re an employee, you receive a W-2. As a W-2 employee, payroll taxes are automatically deducted from your paycheck and then paid to the government through your employer.

What’s the difference between a 1099 MISC and a W-2?

A Form 1099-MISC is the tax form you receive from a company you contracted with. A W-2 is the tax form you receive as an employee from your employer. The major difference between these forms is the tax section.

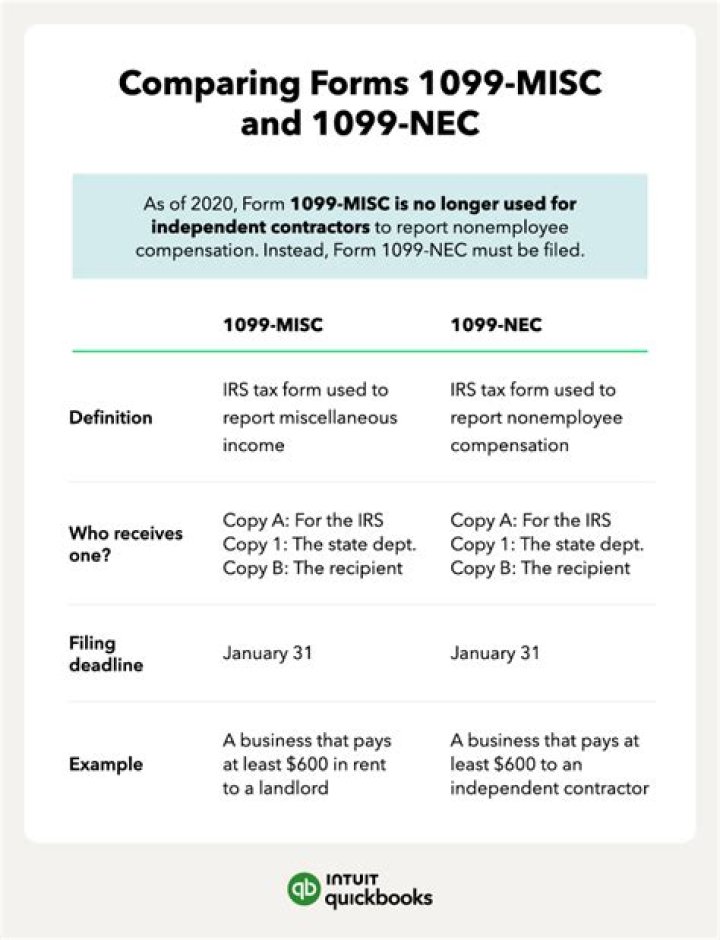

What do you need to know about Form 1099 MISC?

Form 1099-MISC. In the United States, Form 1099-MISC is a variant of Form 1099 used to report miscellaneous income. One notable use of Form 1099-MISC is to report amounts paid by a business (including nonprofits) to a non-corporate US resident independent contractor for services (in IRS terminology, such payments are nonemployee compensation).

Can a payee file both Form 1099 MISC and 1099-K?

As of 2016 this remains a problem. Even with this provision, many payers still choose to file Form 1099-MISC. This means that if the payee meets the minimum threshold for receiving Form 1099-K, they may actually receive both Form 1099-MISC and Form 1099-K and possibly over-report their payments.

What are the penalties for not filing Form 1099 MISC?

Form 1099-Misc needs to be provided for Royalties of $10 or more. If the payer does not file Form 1099-MISC, there is a maximum penalty of $250 per form not filed, up to $500,000 per year. Otherwise for late filings the penalty varies from $30 to $100, depending on how late the filing was.