A grantor trust is a trust in which the individual who creates the trust is the owner of the assets and property for income and estate tax purposes. Grantor trust rules are the rules that apply to different types of trusts. All grantor trusts are revocable living trusts, while the grantor is alive.

Who pays the tax on a grantor trust?

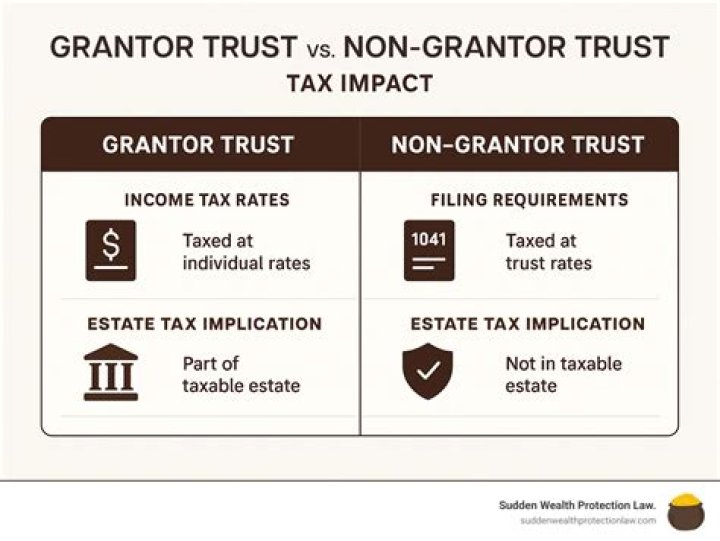

If a trust is a grantor trust, then the grantor is treated as the owner of the assets, the trust is disregarded as a separate tax entity, and all income is taxed to the grantor.

What is the benefit of a grantor trust?

Grantor trusts can provide wealth preservation by giving the assets within the trust certain asset protection, keeping these assets out of the grantor’s estate, and alleviating the burden of tax from the trust assets and the beneficiaries of the trust.

Are there income tax implications for a grantor trust?

The trust that you established for estate planning purposes may have some interesting income tax considerations. Be aware of who pays the income tax on the trust income, the opportunities with grantor trust planning, and the income tax effect and distribution planning opportunities for non-grantor trusts.

Do you pay taxes on an inheritance from a trust?

The type of asset inherited in a trust will also factor into whether you’ll pay tax on an inheritance and how much. This is another reason to discuss the inheritance with your CPA or accountant. If you inherit a retirement account, it will be taxable as ordinary income, often to the beneficiary directly due to the trust tax rates.

What’s the difference between a grantor and non-grantor?

In addition, your trust’s income tax, paid by you as the grantor, is not considered an additional gift to the trust. Basically, the trust assets can grow for the benefit of the beneficiaries, without the economic burden of paying income tax. In essence, this is a tax-free gift.

Is the grantor trust considered a disregarded entity?

A grantor trust is considered a disregarded entity for income tax purposes. Therefore, any taxable income or deduction earned by the trust will be taxed on the grantor’s tax return.