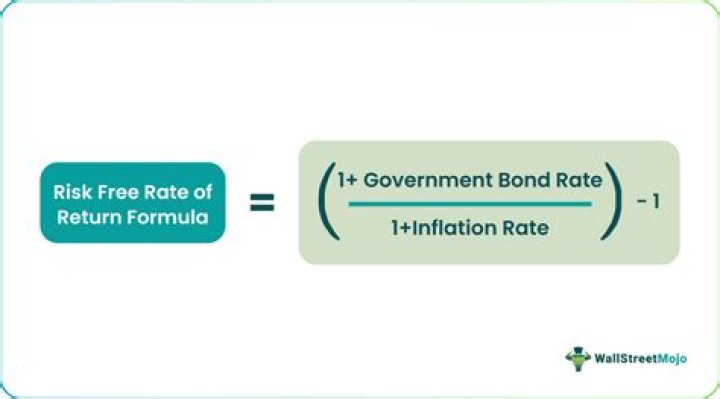

The risk-free rate of return is the theoretical rate of return of an investment with zero risk. The risk-free rate represents the interest an investor would expect from an absolutely risk-free investment over a specified period of time.

How is risk-free rate of return calculated using CAPM?

The amount over the risk-free rate is calculated by the equity market premium multiplied by its beta. In other words, it is possible, by knowing the individual parts of the CAPM, to gauge whether or not the current price of a stock is consistent with its likely return.

What is the expected return for the market according to the CAPM?

What is the expected return of the security using the CAPM formula? Let’s break down the answer using the formula from above in the article: Expected return = Risk Free Rate + [Beta x Market Return Premium] Expected return = 2.5% + [1.25 x 7.5%]

Can market return be less than risk-free rate?

Concepts Used to Determine Market Risk Premium If an investment’s rate of return is lower than that of the required rate of return, then the investor will not invest. It is also called the hurdle rate. Expected market risk premium – based on the investor’s return expectation.

What is a good Sharpe ratio?

Usually, any Sharpe ratio greater than 1.0 is considered acceptable to good by investors. A ratio higher than 2.0 is rated as very good. A ratio of 3.0 or higher is considered excellent. A ratio under 1.0 is considered sub-optimal.

How do you calculate market risk?

The market risk premium can be calculated by subtracting the risk-free rate from the expected equity market return, providing a quantitative measure of the extra return demanded by market participants for the increased risk. Once calculated, the equity risk premium can be used in important calculations such as CAPM.

How is risk premium calculated?

The risk premium is calculated by subtracting the return on risk-free investment from the return on investment. Risk Premium formula helps to get a rough estimate of expected returns on a relatively risky investment as compared to that earned on a risk-free investment.

How do I buy a 3 month treasury bill?

You can buy Treasury bills directly from the U.S. Treasury via TreasuryDirect, or you can buy them in a brokerage account. The top 3 brokerage firms Vanguard (on the brokerage platform), Fidelity, and Schwab all sell new-issue Treasury bills with no fee whatsoever.

Why is unsystematic risk ignored?

Why do not we consider unsystematic risk while calculating CAPM? – Quora. It’s because the model assumes firm-specific risks are (1) random so that we could use variance to measure risks, (2) independent so that the covariance between them is zero and (3) investors can diversify themselves by holding many stocks.