Planned detection risk is the risk that audit evidence will fail to detect misstatements that exceed a tolerable amount. An increase in planned detection risk may be caused by an increase in acceptable audit risk or a decrease in control risk or inherent risk.

What increases audit risk?

Your audit risk increases if the deduction is taken on a return that reports a Schedule C loss and/or shows income from wages.

What is an acceptable audit risk?

Acceptable audit risk is the risk that the auditor is willing to take of giving an unqualified opinion when the financial statements are materially misstated. As acceptable audit risk increases, the auditor is willing to collect less evidence (inverse) and therefore accept a higher detection risk (direct).

What is the formula for audit risk?

Audit risk can be calculated as: AR = IR × CR × DR.

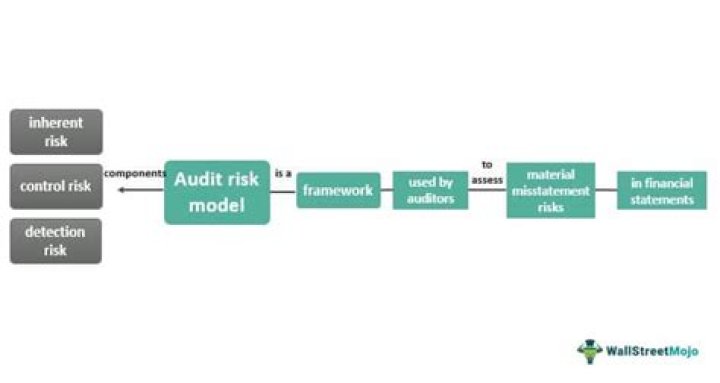

Which is the last of the three audit risk components?

Detection risk is considered the last one of the three audit risk components. This is due to without proper assessment of inherent and control risk, auditors would have no basis for assessing the detection risk. And as a result, auditors would not be able to properly plan the nature, timing and extent of the audit procedures.

When does an auditor do a risk assessment?

Auditor requires to perform risk assessments to make sure that all possible risks of misstatements that might happen to the financial statements are identified. This is normally performed during and after the audit plan.

How is control risk related to audit risk?

Basically, if the control is weak, there is a high chance that financial statements are materially misstated, and there is subsequently a high chance that auditors could not detect all kinds of those misstatements. That means to control risk could lead to audit risk. Don’t be confused that it is the detection risk.

How does an auditor deal with inherent risk?

Also, auditors cannot change or influence inherent risk; hence, the only way to deal with inherent risk is to tick it as high, moderate or low and perform more audit procedures to reduce the level of audit risk.