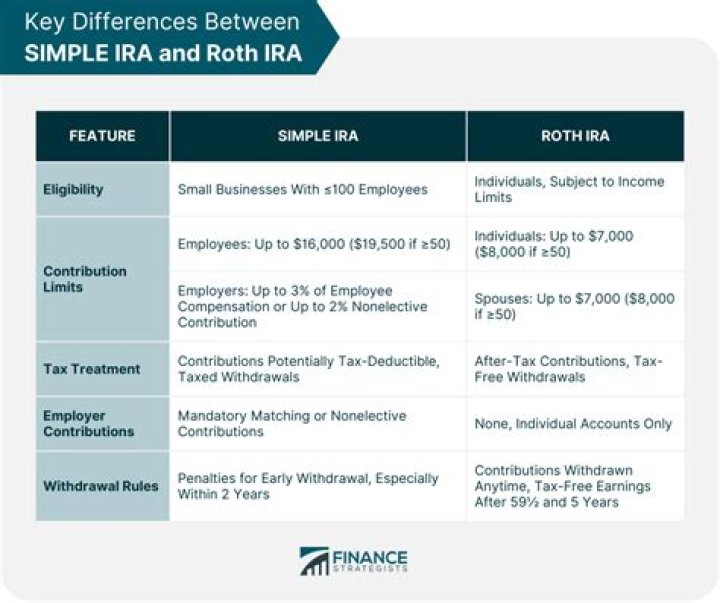

All employees who received at least $5,000 in compensation from you during any 2 preceding calendar years (whether or not consecutive) and who are reasonably expected to receive at least $5,000 in compensation during the calendar year, are eligible to participate in the SIMPLE IRA plan for the calendar year.

Can I have 2 simple IRAs?

There is no limit to the number of IRA plans that an employee can establish, but you will be subject to annual contribution limits. You cannot max all of them out, as the limits are set for the sum total of all of your IRA accounts.

How does a SIMPLE IRA work for an employer?

In a Simple IRA plan, the employer establishes an individual Traditional IRA account for each of his or her employees. Both the employer and employees can then contribute to these accounts, earning tax benefits both at the time of the contribution and later, by deferring income taxes on the profits earned on the assets in the account.

Do you have to pay taxes on SIMPLE IRA?

With a SIMPLE IRA, you and your employees can put a percentage of pay aside for retirement. The money will grow tax-deferred until it’s withdrawn at retirement. So, you won’t have to pay taxes on your investment growth, but you will have to pay income taxes when you take out money.

Are there limits on how much an employer can contribute to SIMPLE IRA?

On the plus side, the required contribution amounts are capped at only 3% of an employee’s compensation and may not be costly for an employer with a small number of employees, especially if the employees’ compensation amounts are low. An employer can choose between two options for making contributions to the SIMPLE IRA Plan.

Are there any downsides to a SIMPLE IRA?

A second downside of the SIMPLE IRA is that they cannot be held in conjunction with other employer-sponsored plans. This means that if you want to reward a specific set of highly compensated employees with a profit sharing plan bonus, you’ll need to establish a 401 (k) or Safe Harbor 401 (k) instead of a SIMPLE IRA.