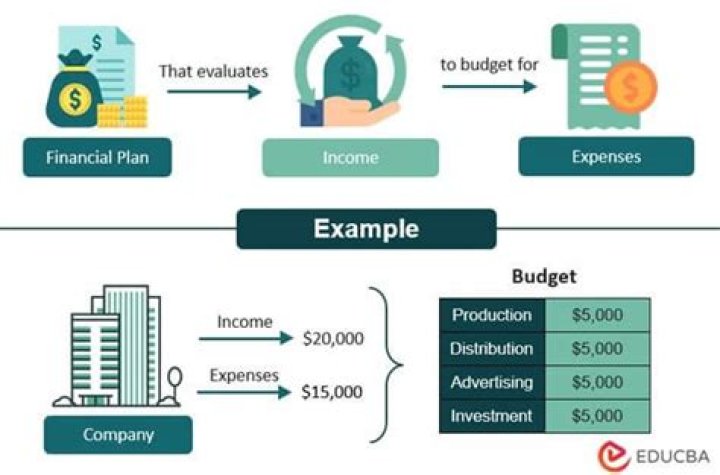

A budget is a tool that managers use to plan and control the use of scarce resources. A budget is a plan showing the company’s objectives and how management intends to acquire and use resources to attain those objectives.

Why is budgeting important managerial accounting?

An important step in the initiation of the company’s strategic plan is the creation of a budget. A good budgeting system will help a company reach its strategic goals by allowing management to plan and to control major categories of activity, such as revenue, expenses, and financing options.

How does management accounting help in planning?

Management accounting helps managers in planning by providing reports which estimate the effects of alternative actions on an enterprise’s ability to achieve desired goals. As part of the budgeting process, management accountants prepare budgeted (forecasted) financial statements, often called proforma statements.

How do you create a budget in management accounting?

Here are the basic steps to follow when preparing a budget:

- Update budget assumptions.

- Review bottlenecks.

- Available funding.

- Step costing points.

- Create budget package.

- Issue budget package.

- Obtain revenue forecast.

- Obtain department budgets.

What is the first step in the budget process?

Six steps to budgeting

- Assess your financial resources. The first step is to calculate how much money you have coming in each month.

- Determine your expenses. Next you need to determine how you spend your money by reviewing your financial records.

- Set goals.

- Create a plan.

- Pay yourself first.

- Track your progress.

What does Managerial Accounting consist of?

Managerial accounting encompasses many facets of accounting, including product costing, budgeting, forecasting, and various financial analysis.

What are the three major activities of a manager?

Most of the job responsibilities of a manager fit into one of three categories: planning, controlling, or evaluating. The model in Figure 1.2 sums up the three primary responsibilities of management and the managerial accountant’s role in the process.