Base erosion payment. A base erosion. payment is any amount paid or accrued by. a taxpayer to a foreign person (as defined. in Regulations section 1.59A-1(b)(10)) that is a related party (as defined in.

How is base erosion tax benefit calculated?

The Base Erosion Percentage for a taxable year is calculated by dividing: the aggregate amount of Base Erosion Tax Benefits (the “numerator”) by. the sum of the aggregate amount of deductions plus certain other Base Erosion Tax Benefits (the “denominator”).

Is interest a base erosion payment?

Interest on direct allocations and on US-booked liabilities paid or accrued to a foreign related party would be a base erosion payment. Interest on excess US-connected liabilities may also be a base erosion payment if the foreign corporation has liabilities with a foreign related party.

How do you calculate base erosion percentage?

The base erosion percentage for any tax year generally equals the total base erosion tax benefits for the year (the numerator) divided by the total deductions for the year (including base erosion tax benefits) but excluding deductions allowed under IRC Sections 172, 245A or 250, and certain other deductions that are …

Is interest a beat payment?

The BEAT targets large US corporations that make deductible payments, such as interest, royalties, and certain service payments, to related foreign parties. However, the BEAT excludes payments that can be treated as cost of goods sold.

How is beat calculated?

The BEAT is calculated on the excess of modified taxable income over a taxpayer’s regular tax liability, reduced by certain types of credits. The 2020 Final Regulations are very similar to the 2019 Proposed Regulations, with a few important changes. One modification relates to the deemed closing of a taxable year.

What are benefits limitations?

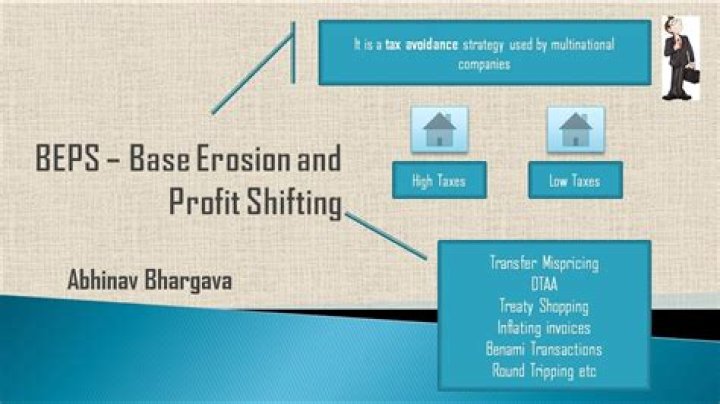

Limitation on benefits clauses are drafted with the intention of avoiding treaty shopping, whereby a third-party national or corporation sets up a shell company in a contracting state through which income will be passed by the owners in an attempt to achieve a minimal tax rate, or to eliminate tax on the income …

What is a company that meets the base erosion test?

Company that meets the ownership and base erosion test – this test generally requires that more than 50% of the vote and value of the company’s shares be owned, directly or indirectly, by individuals, governments, tax-exempt entities, and publicly-traded corporations resident in the same country as the company, as long …

When do you have to pay base erosion tax?

Under Code Sec. 59A, with respect to base erosion payments (as defined below) paid or accrued in tax years that begin after Dec. 31, 2017, “applicable taxpayers” are required to pay a tax, the “base erosion anti-abuse tax” (BEAT), equal to the “base erosion minimum tax amount” for the tax year. (Code Sec. 59A (a))

Which is an example of a base erosion payment?

For example, any premium or other consideration paid or accrued by a taxpayerto a foreign related partyfor any reinsurance paymentsis not reduced by or netted against other amountsowed to the taxpayerfrom the foreign related partyor by reserve adjustmentsor other returns. (iv)Amounts paid or accrued with respect to mark-to-market position.

Can a service company be excluded from base erosion?

Effectively, any portion of base erosion payments that can rightfully be considered COGs may be excluded, meaning that the taxpayer is not penalized (i.e., BEAT does not apply) on that portion. For services companies, however, the costs inherent in providing the services are costs of services, not COGs.

What is the minimum amount for base erosion?

( Code Sec. 59A (e) (3)) The base erosion minimum tax amount equals the excess of: a) a statutory percentage of the taxpayer’s modified taxable income over b) the taxpayer’s regular tax liability reduced by certain excess credits.