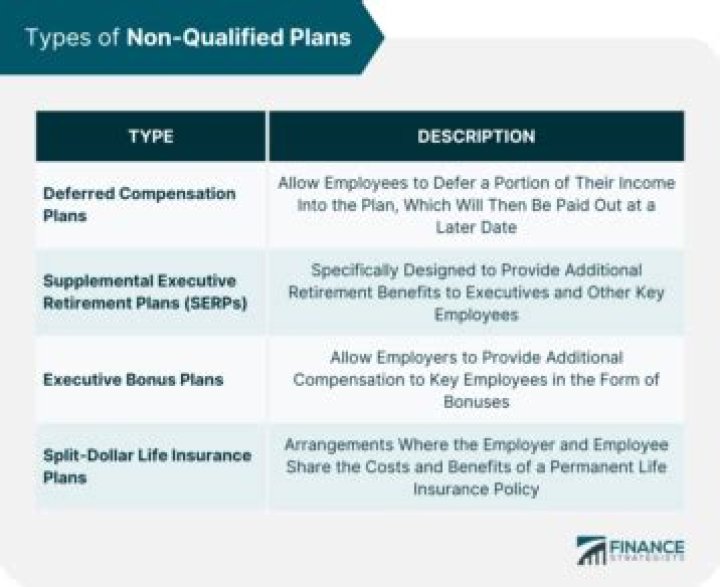

Nonqualified plans are retirement savings plans. They are called nonqualified because unlike qualified plans they do not adhere to Employee Retirement Income Security Act (ERISA) guidelines. Nonqualified plans are generally used to provide high-paid executives with an additional retirement savings option.

How do I set up a non-qualified deferred compensation plan?

To set up a NQDC plan, you’ll have to: Put the plan in writing: Think of it as a contract with your employee. Be sure to include the deferred amount and when your business will pay it. Decide on the timing: You’ll need to choose the events that trigger when your business will pay an employee’s deferred income.

Is a non-qualified deferred compensation plan a good idea?

NQDC’s are especially good for employees who are already maxing out their qualified plans, such as 401(k) plans. NQDC plans can exist in the form of stock options and retirement plans.

What is a nonqualified plan on w2 Box 11?

The non-qualified plan on a W-2 is a type of retirement savings plan that is employer-sponsored and tax-deferred. They are non-qualified because they fall outside the Employee Retirement Income Security Act (ERISA) guidelines and are exempt from the testing required with qualified retirement savings plans.

Is deferred compensation a non qualified pension plan?

Because NQDC plans are not qualified, meaning they aren’t covered under the Employee Retirement Income Security Act (ERISA), they offer a greater amount of flexibility for employers and employees.

What do you call a nonqualified deferred compensation plan?

NQDC plans (sometimes known as deferred compensation programs, or DCPs, or elective deferral programs, or EDPs) allow executives to defer a much larger portion of their compensation and to defer taxes on the money until the deferral is paid. Explore our 3-part series on making the most of nonqualified deferred compensation plans.

What does it mean to have a non-qualified benefit plan?

Non-qualified plans are employee benefit plans that do not meet ERISA guidelines, leaving a more flexible plan with a variety of possibilities for employees.

Do you have a non qualified distribution plan?

Read Viewpoints on Fidelity.com: Non-qualified distribution investing and Distribution strategies delve into how to approach those decisions. But before you tackle these issues, you must first decide whether to participate in your company’s NQDC plan at all.

Can a NQDC plan be an unfunded plan?

There are several varieties of NQDC plans (also called 409A plans after the section in the tax code governing them, introduced in 2004); the one discussed here is the basic unfunded plan for deferring part of annual compensation (the most common type). 1 The tax law requires the plan to meet all of the following conditions: