The deferred loss is a deduction when calculating any net profit or loss from the activity in that future year.

What is the difference between deferred and accrued?

Deferred revenue, also known as unearned revenue, refers to advance payments a company receives for products or services that are to be delivered or performed in the future. Accrued expenses refer to expenses that are recognized on the books before they have actually been paid.

Is Deferred Income A accrual?

When considering cash flows, there are differences between deferred and accrued revenues. Deferred income involves receipt of money, while accrued revenues do not – cash may be received in a few weeks or months or even later.

How long can you defer a capital loss?

You can’t deduct a capital loss from your assessable income, but in most cases it can be used to reduce a capital gain you made in 2019–20. If you made no capital gain in 2019–20, defer the capital loss until you make a capital gain.

What is the journal entry for deferred income?

You need to make a deferred revenue journal entry. When you receive the money, you will debit it to your cash account because the amount of cash your business has increased. And, you will credit your deferred revenue account because the amount of deferred revenue is increasing. Date. Account.

How is deferred revenue added to an accrual sheet?

The relaxation is added to deferred revenue (liability) on the steadiness sheet for that yr. Deferred earnings (also called deferred income, unearned income, or unearned revenue) is, in accrual accounting, cash earned for goods or companies which haven& #39 ;t yet been delivered.

What kind of expenses are not included in deferred revenue?

Common prepaid expenses may include monthly rent or insurance payments that have been paid in advance. Since deferred revenues are not considered revenue until they are earned, they are not reported on the income statement.

How does deferred revenue work in a SaaS business?

Categorizing deferred revenue as earned on your income statement is aggressive accounting which will overstate your sales revenue. SaaS businesses follow the accrual accounting method. ASC 606 / IFRS 15 are the key accounting principles that must be followed.

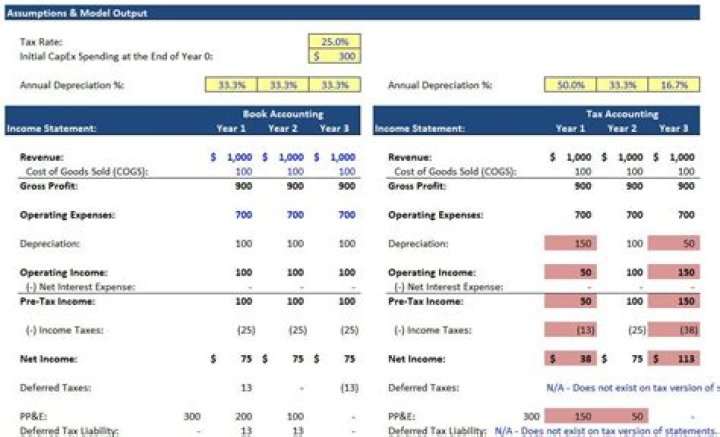

How are deferred tax assets and liabilities calculated?

Deferred tax assets/liabilities are computed using the substantiality enacted tax rate on such temporary differences which are either taxable or deductible in future periods, subject to specific exemptions under Ind AS 12. Temporary differences are either taxable temporary differences or deductible temporary differences.