All deductions work by cutting your taxable income, and lower taxable income means less taxes owed for you. Deductions are intentional loopholes, written into the tax code to give you a break for certain financial and life circumstances.

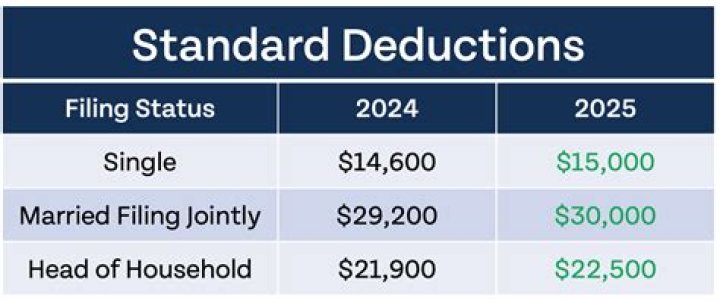

What exactly is the standard deduction?

The standard tax deduction is a flat amount that the tax system lets you deduct, no questions asked. Tax deductions allow individuals and companies to subtract certain expenses from their taxable income, which reduces their overall tax bill. That flat amount is called a “standard deduction.”

What is difference between standard deduction and itemized deduction?

The difference between the standard deduction and itemized deduction comes down to simple math. The standard deduction lowers your income by one fixed amount. On the other hand, itemized deductions are made up of a list of eligible expenses. You can claim whichever lowers your tax bill the most.

How are bundled fees deductible on a 1040?

Bundled fees are fees that are billed together, where a portion is fully deductible and another is subject to the 2%-of-AGI floor. The proposed regulations would require the deductible and nondeductible portions to be “unbundled”—that is, allocated between costs that are subject to the 2% floor and those that are not.

When does the 2% floor on miscellaneous deductions apply?

The IRS issued final regulations on the controversial question of which costs incurred by trust and estates are subject to the 2% floor on miscellaneous deductions under Sec. 67 (a) (T.D. 9664). The regulations will apply to tax years beginning on or after May 9, 2014.

How are estate administrative expenses treated on Form 1040?

The Supreme Court held that the latter provision limits its treatment to expenses that would not “commonly” or “customarily” be incurred if the property were held by an individual.

How are trust expenses classified as miscellaneous itemized deductions?

Because the trust is a grantor trust, all of the income and expenses are attributable to Beneficiary A even though no distributions were made from the trust. The trust expenses for trustee, legal, accounting and investment advisory fees are categorized as “miscellaneous itemized deductions ” subject to the 2% floor to the beneficiary .