The credit card charge-off rate is a measure that shows the percentage of defaulted credit card balances in comparison to the total amount of credit outstanding. Credit card companies track credit card charge-off rates to monitor the performance of their credit card loans.

What is a charge-off ratio?

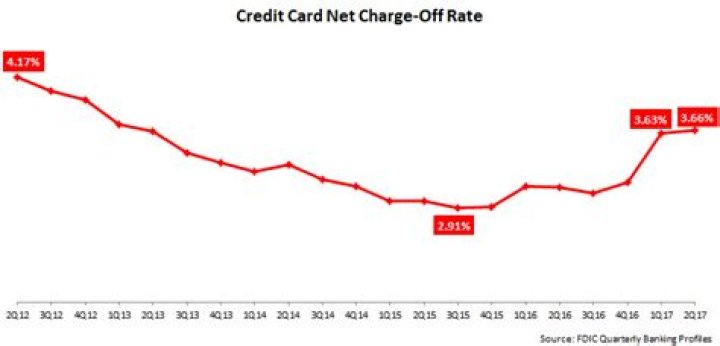

The net charge-off rate is the annualized ratio of net charge-offs (NCOs) to average loans outstanding. NCOs are a lender’s gross charge-offs less recoveries of its delinquent debt. The net charge-off rate measures the proportion of debt owed to a company that is unlikely to be paid back to that company.

How do you calculate charge-off?

The Calculation of Charge-off Rates Charge-off rates for any category of loan are defined as the flow of a bank’s net charge-offs (gross charge-offs minus recoveries) during a quarter divided by the average level of its loans outstanding over that quarter.

When do you have to charge off a credit card?

The term can be used in conjunction with various types of debt, such as that originating from a credit card, mortgage, auto loan, etc. Banks are legally required to charge-off debt when it reaches a certain level of delinquency, which varies by the type of debt.

Can a credit card company remove a charge off from your credit report?

Credit card companies are contractually bound to report credit information to the credit bureaus, so it can be difficult to get a creditor to agree to remove the charge-off from your credit report. Even so, some cardholders have been successful in making a pay for delete agreement.

How long does a charge off stay on your credit report?

If you applied for a credit card in the months leading up to your charge-off, your application may have been denied. Once a charge-off is on your credit report, it will remain there for seven years from the date it was charged off. In total, the account remains on your credit report for seven and a half years.

How does a charge off affect my credit score?

A charge-off ranks just below a bankruptcy in impact in terms of scoring damage. Whether the account went to inside collections or was sold to an outside collector makes no difference to your score. It’s all the same account and the same delinquency. So you only get a negative hit to your score for a single charge-off once.