In the broadest definition, business expenditure is the money you spend ‘wholly and exclusively’ for your business. This definition is simple to apply when you incur a cost exclusively for your business, e.g. office supplies.

What should business expenses include?

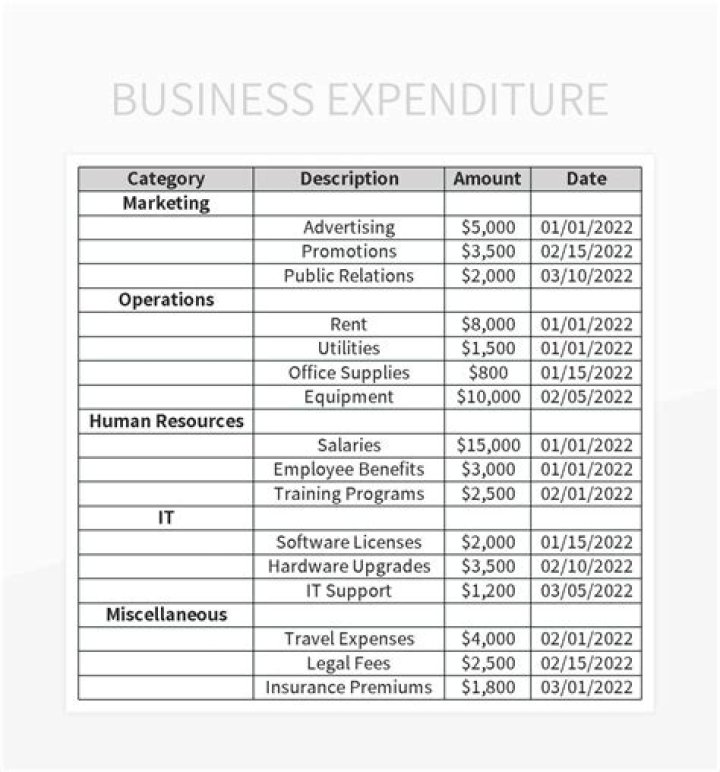

Business expenses list

- Rent or mortgage payments.

- Office equipment.

- Payroll costs (e.g., wages, benefits, and taxes)

- Advertising and marketing.

- Utilities.

- Small business insurance.

- Depreciation.

- Taxes.

Can you claim business set up costs?

Under normal circumstances startup costs are regarded as a capital cost of a business and not tax-deductible. Because you are conducting your business from home, unless you can find a way that substantiates your claim for electricity and gas related to running the business, you cannot claim these costs.

What are the different types of expenditure in business?

To sum up: 1 Expenditure refers to payments made or liabilities incurred in exchange for goods or services. 2 Expenditure increases the value of assets or reduces a liability 3 The three types of expenditure that a business can incur include capital expenditure, revenue expenditure, and deferred revenue expenditure 更多结果…

When is expenditure incurred after set up of business allowable?

When the business of the assessee is held set up and commenced during the year, the expenditure of Rs. 67,57,190/- is no longer constitutes ‘pre-operative’ expenditure which is capital in nature and therefore, the same becomes an allowable expenditure.

How many budgets do you need for a small business?

Decide how many budgets you really need. Many small businesses have one overall operating budget which sets out how much money is needed to run the business over the coming period – usually a year. As your business grows, your total operating budget is likely to be made up of several individual budgets such as your marketing or sales budgets.

What are the rules for disallowance of Business expenditure?

9) Sec. 40 A(3): Where any expenditure in respect of which payment is made in excess of Rs. 20,000 at a time otherwise than by Account-payee cheque or draft, 100% of such payment shall be disallowed.