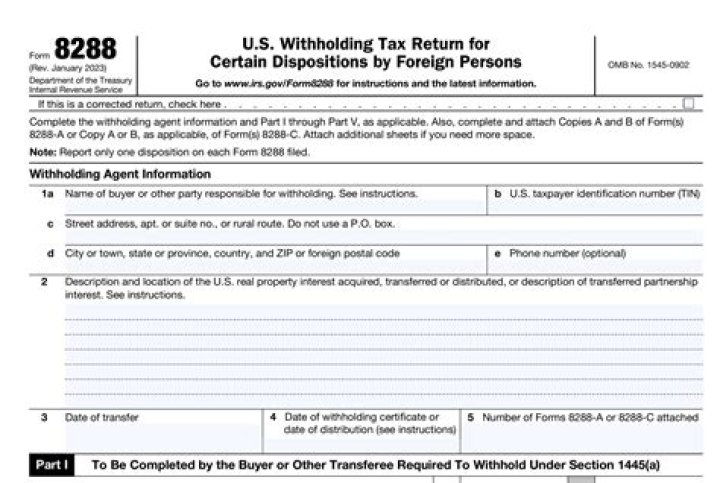

Form 8288. The tax withheld on the acquisition of a U.S. real property interest from a foreign person is reported and paid using Form 8288. If the principal purpose of applying for a withholding certificate is to delay paying over the withheld tax to the IRS, the transferee will be subject to interest and penalties.

What is a Notice 1445 from the IRS?

The disposition of a U.S. real property interest by a foreign person (the transferor) is subject to income tax withholding (IRC section 1445). The transferee is the withholding agent. If the transferor is a foreign person and you fail to withhold, you may be held liable for the tax.

How can I get a copy of my IRS Notice?

You can get it on IRS.gov or by calling 800-TAX-FORM (800-829-3676).

How does the IRS send a Form 8288?

IRS will stamp copy B of Form 8288-A and send it to the transferor, the person subject to withholding. The transferor must file a U.S. income tax return and attach the stamped Form 8288–A to receive credit for any tax withheld. CAUTION!

What happens if my tin is not included in Form 8288?

Transferor’s TIN missing. If you do not have the transferor’s taxpayer identification number (TIN), you still must file Forms 8288 and 8288-A. A stamped copy of Form 8288-A will not be provided to the transferor if the transferor’s TIN is not included on that form.

How to apply for a Withholding Certificate from the IRS?

You can complete this procedure by submitting a completed IRS form 8288-B and the seller or buyer, also known as the transferor or transferee can both apply for the withholding certificate. What Is The Purpose Of A Withholding Certificate?

Who must file amount to withhold Internal Revenue Service?

Who Must File A buyer or other transferee of a U.S. real property interest, and a corporation, qualified investment entity, or fiduciary that is required to withhold tax, must file Form 8288 to report and transmit the amount withheld. If two or more persons are joint transferees, each is obligated to withhold.