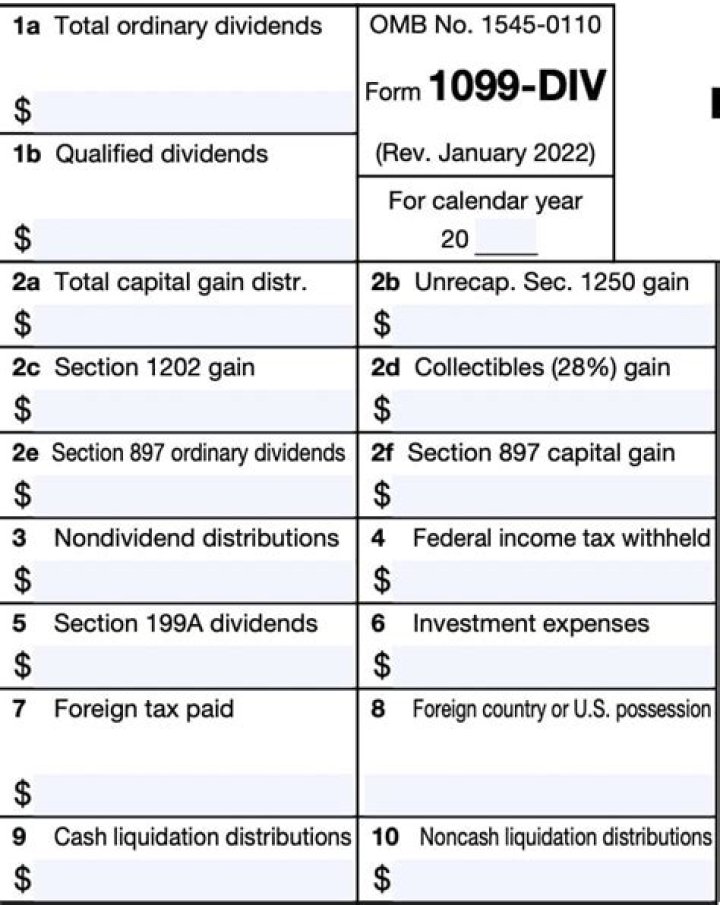

Section 199A dividends are dividends from domestic real estate investment trusts (“REITs”) and mutual funds that own domestic REITs. These dividends are reported on Form 8995 or Form 8995-A and qualify for the Section 199A QBI deduction.

Do I need to report my 1099-DIV?

Even if you don’t received a Form 1099-DIV, you are required to still report all of your taxable dividend income. Schedule B is necessary when the total amount of dividends or interest you receive exceeds $1,500.

What is tax Form 1099-DIV?

Form 1099-DIV: Dividends and Distributions is an Internal Revenue Service (IRS) form sent by banks and other financial institutions to investors who receive dividends and distributions from any type of investment during a calendar year. Investors can receive multiple 1099-DIVs.

Where do I report my section 199A dividends?

These dividends are reported on Form 8995 or Form 8995-A and qualify for the Section 199A QBI deduction. The good news is that the taxpayer (generally) gets a federal income tax deduction equal to 20 percent of the amount in Box 5.

What do you need to know about Form 1099 Div?

A Form 1099-DIV is a great window into your taxable investments. By learning how to read the major boxes of your 1099-DIV, you can gain valuable insights about your investments and their tax efficiency. Form 1099-DIV exists so that taxpayers and the IRS know the income generated by financial assets in dividend paying accounts.

What is box 13-15 on form 1099-DIV?

Box 13 – 15 contains the State Withholding Information related to the bond or other debt investment. To input the Form 1099-DIV, Box 1a through Box 6 and Nominee Dividends, amount of interest on U.S. Savings Bonds and Treasury Obligations amounts in, from the Federal Section:

Where can I find the 1961 income tax form?

Form of application for allotment of Tax Deduction and Collection Account Number under section 203A of the Income-tax Act, 1961 Form of declaration to be filed by a person who does not have a permanent account number and who enters into any transaction specified in rule 114B