Because depreciation is accelerated, expenses are higher in earlier periods compared to later periods. Companies may utilize this strategy for taxation purposes, as an accelerated depreciation method will result in a deferment of tax liabilities since income is lower in earlier periods.

Can you accelerate depreciation?

There are two ways to accelerate the depreciation schedule of an asset. This system lets you deduct a higher percentage of an asset’s cost during its early years of use. The other option is to elect the Section 179 deduction for your purchases.

What is meaning of accelerated depreciation?

Accelerated depreciation definition Accelerated depreciation is a method used to calculate asset value over time. It’s based on the principle that an asset’s value is highest at the beginning of its lifespan, allowing for more significant depreciation in value during these first few years.

Do companies prefer straight-line or accelerated depreciation?

Straight-line depreciation is easier to calculate and looks better for a company’s financial statements. This is because accelerated depreciation shows less profit in the early years of asset acquisition.

Why do you use accelerated depreciation for taxes?

Accelerated depreciation is a depreciation method whereby an asset loses book value at a faster rate than the traditional straight-line method. Generally, this method allows greater deductions in the earlier years of an asset and is used to minimize taxable income.

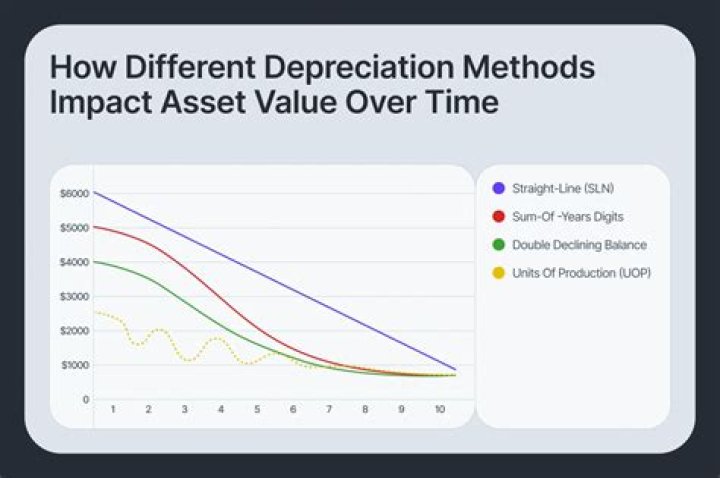

What’s the difference between straight line and accelerated depreciation?

While the straight-line depreciation method spreads the cost evenly over the life of an asset, an accelerated depreciation method allows the deduction of higher expenses in the first years after purchase and lower expenses as the depreciated item ages.

Is the double declining method an accelerated depreciation method?

The double declining method is an accelerated depreciation method. After taking the reciprocal of the expected life of the asset and doubling it, this rate is applied to the depreciable base for the remainder of the asset’s expected life.

Are there any changes to accelerated depreciation for 2017?

The 2017 Tax Cuts and Jobs Act made changes to extend several accelerated depreciation benefits for businesses: A permanent $500,000 limit on Section 179 deductions will allow businesses to plan for asset purchases and expense purchases immediately instead of depreciating over a period of time.