While few people are actually prosecuted criminally, the IRS does routinely impose the civil penalties for willful failure to file FBAR. The penalties for a willful violation are the greater of $124,588 or 50% of the account value at the time of the violation.

What is a delinquent FBAR?

The FBAR is the Report of Foreign Bank and Financial Account Form (FinCEN Form 114). The failure to report the form timely may result in significant fines and penalties. The delinquent FBAR procedures require the Account Holder to have the limited issue of delinquent FBAR filing.

Who must file FBAR 2021?

Who has to file an FBAR in 2021? The FBAR rules state that any American who has a total of over $10,000 in foreign financial accounts at any time during 2020 must report all of their foreign accounts by filing an FBAR in 2021.

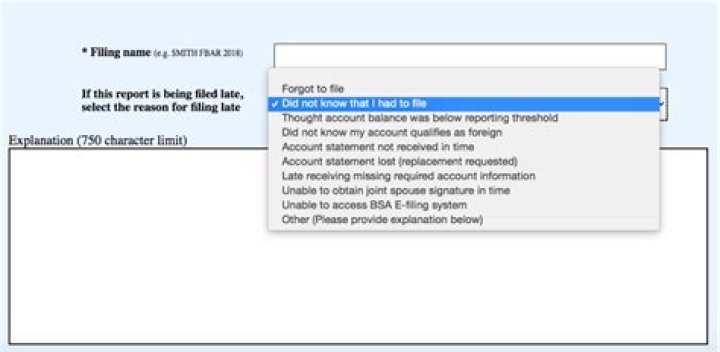

How to contact FinCEN for delinquent FBAR submission?

On the cover page of the electronic form, select a reason for filing late. If you are unable to file electronically, contact FinCEN’s Regulatory Help line at 1-800-949-2732 or 1-703-905-3975 (if calling from outside the United States) to determine possible alternatives to electronic filing.

When do you have to file a FBAR?

U.S. persons must file FBARs if the aggregate value of their foreign financial accounts exceeds $10,000 at any point during the tax year. The penalty for willful failure to file the FBAR is the greater of 50 percent of the account balance or $129,210. Even a non-willful failure to file a FBAR may result in a $12,921 penalty. 3

Is there penalty for failure to file delinquent FBAR?

The IRS will not impose a penalty for the failure to file the delinquent FBARs if you properly reported on your U.S. tax returns, and paid all tax on, the income from the foreign financial accounts reported on the delinquent FBARs, and you have not previously been contacted regarding an income tax examination or a request for delinquent returns …

What does FBAR stand for in Title 31?

The obligation to file an FBAR is derived from Title 31 of the U.S. Code, specifically 31 U.S.C. § 5314, which requires U.S. persons to maintain records and file reports with respect to that person’s financial accounts held at a foreign financial institution. Title 31 deals with monetary instruments, including topics such as money laundering.