The equilibrium price is the only price where the plans of consumers and the plans of producers agree—that is, where the amount consumers want to buy of the product, quantity demanded, is equal to the amount producers want to sell, quantity supplied. This common quantity is called the equilibrium quantity.

How is market equilibrium achieved?

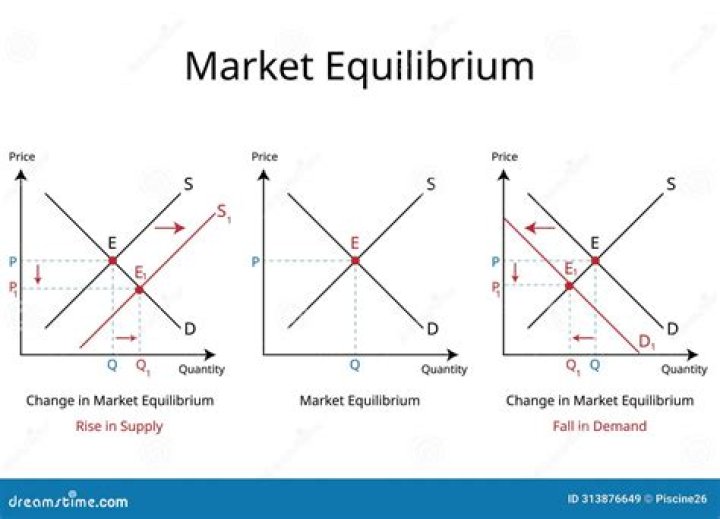

MARKETS: Equilibrium is achieved at the price at which quantities demanded and supplied are equal. We can represent a market in equilibrium in a graph by showing the combined price and quantity at which the supply and demand curves intersect.

Why does market equilibrium cause stable prices?

In the case of excess demand, sellers will quickly run down their stocks, which will trigger a rise in price and increased supply. The more efficiently the market works, the quicker it will readjust to create a stable equilibrium price.

What happens if price is below equilibrium?

If the market price is below the equilibrium price, quantity supplied is less than quantity demanded, creating a shortage. The market is not clear. It is in shortage. If a shortage exists, price must rise in order to entice additional supply and reduce quantity demanded until the shortage is eliminated.

What is market equilibrium with example?

Definition of market equilibrium – A situation where for a particular good supply = demand. When the market is in equilibrium, there is no tendency for prices to change. We say the market-clearing price has been achieved. A market occurs where buyers and sellers meet to exchange money for goods.

How do you maintain market equilibrium?

Once you raise the price of your product, your product’s quantity demanded will drop until equilibrium is reached. Therefore, shortage drives price up. If a surplus exist, price must fall in order to entice additional quantity demanded and reduce quantity supplied until the surplus is eliminated.

Is market price and equilibrium price the same?

The key difference between market price and equilibrium price is that market price is the economic price for which a good or service is offered in the marketplace whereas equilibrium price is the price where demand and supply for a good or service are equal.