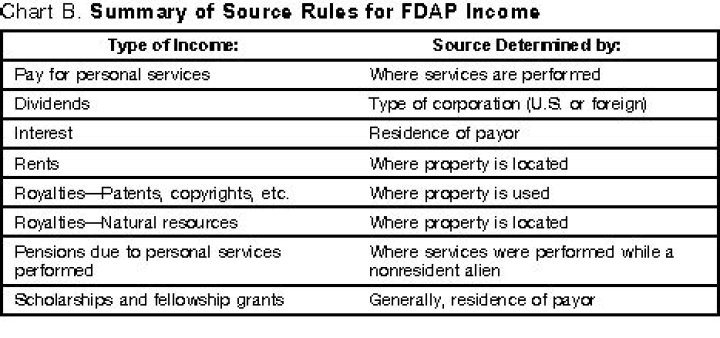

Generally, NRA withholding describes the withholding regime that requires 30% withholding on a payment of U.S. source income and the filing of Form 1042 and related Form 1042-S. Payments to all foreign persons, including nonresident alien individuals, foreign entities and governments, may be subject to NRA withholding.

Why do people not trust the NRA anymore?

“Even if half of what has been reported is correct, it’s still a terrible violation of trust by members of the NRA. The people that are in charge are very powerful and they’ve run roughshod over it and they’ve buried what has happened.

Who is in charge of the NRA now?

LaPierre, in charge of the NRA’s day-to-day operations for nearly three decades, stands accused of spending millions of dollars on luxury black car services and private jet trips, including eight visits to the Bahamas, as well as accepting expensive gifts such as African safaris, hair and makeup for his wife and use of a 107-foot yacht.

Why was Chris Cox kicked out of the NRA?

North, a retired lieutenant colonel infamous for the Iran-Contra scandal of the 1980s, exited the NRA accusing LaPierre of behaving like a dictator. Chris Cox, the NRA’s longtime lobbyist, quit after being accused of working behind the scenes with North to undermine LaPierre.

When does a company have NRA reporting responsibility?

Answer 1: When a company makes a payment of U.S. sourced fixed or determinable annual or periodic (FDAP) income to a foreign person not associated with such person’s U.S. trade or business that company may have an NRA reporting or withholding responsibility.

How much can a NRA give per year?

NRAs also may give up to $15,000 per year without triggering a U.S. gift tax of U.S. situs assets. However, NRAs are not eligible for the $10 million gift and estate tax exemption. They are limited to $60,000 for life.

Are there any tax exemptions for NRAS in USA?

However, NRAs are not eligible for the $10 million gift and estate tax exemption. They are limited to $60,000 for life. Estate and gift tax treaties can affect residency status for non-U.S. citizens and also limit the kinds of property taxed by the U.S.