A tax deduction lowers your taxable income and thus reduces your tax liability. You subtract the amount of the tax deduction from your income, making your taxable income lower. The lower your taxable income, the lower your tax bill.

Who is liable to income tax liability?

Who needs to pay Income Tax? Under existing rules of the IT Act, any individual/business with income irrespective of the amount earned is liable to file income tax returns. But, currently tax on income is payable only if the net taxable income for a fiscal exceeds Rs. 2.5 lakh.

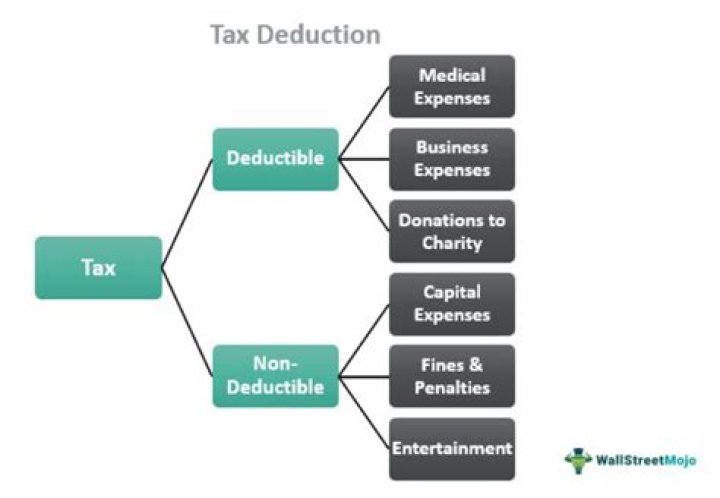

What are the deductions under income tax?

Deductions on Section 80C, 80CCC, 80CCD & 80D

- Section 80C. Investments.

- Section 80CCC. Insurance Premium.

- Section 80CCD. Pension Contribution.

- Section 80TTA. Interest on Savings Account.

- Section 80GG. House Rent Paid.

- Section 80E. Interest on Education Loan.

- Section 80EE. Interest on Home Loan.

- Section 80D. Medical Insurance.

Why are deductions made for income tax?

Deductions reduce your Gross Income. These are the amounts Income Tax Department allows you to reduce your Income, bringing down your tax liability. The more you make use of the deductions allowed, the lower your tax shall be. Deductions are allowed under section 80 of the Income Tax Act (Section 80C to 80U).

What kind of deductions can I claim on my tax return?

Show print controls. Income and deductions Income tax is paid on money you receive, such as salary and wages, Centrelink payments, investment income from rent, interest and dividends, and profits from selling shares or property. You can reduce the amount of tax you pay by claiming certain deductions that are directly related to earning your income.

How does a tax deduction affect your tax return?

Deductions can reduce the income tax that you pay on the money you receive. Most deductions you can claim directly relate to earning your employment income (salary and wages). Your tax payable may also reduce if you are eligible for certain tax offsets or government rebates.

What makes a business expense a tax deduction?

When deductible, they reduce your taxable income and the amount of tax you need to pay. Generally, deductible business expenses are those ‘wholly and exclusively incurred in the production of income’.

Can You claim adjusted gross income before the standard deduction?

Some tax deductions can be claimed before the standard deduction or itemizing. They’re adjustments to income and determine your adjusted gross income.