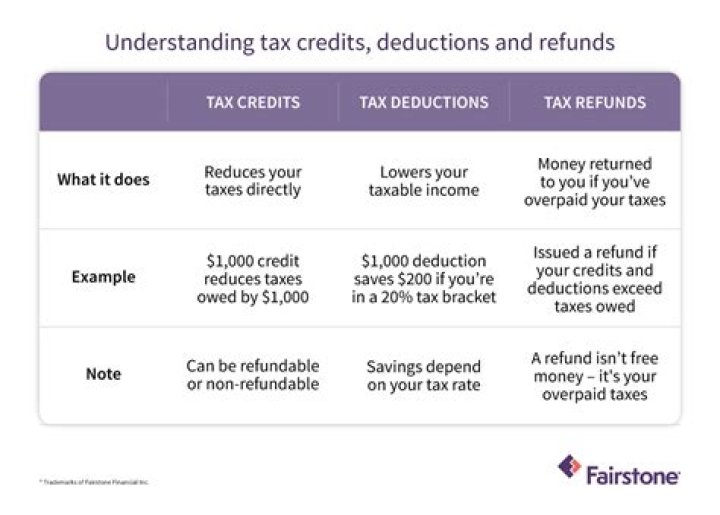

A tax credit is a dollar-for-dollar reduction of the income tax you owe. Tax credits reduce the amount of income tax you owe to the federal and state governments. In most cases, credits cover expenses you pay during the year and have requirements you must satisfy before you can claim them.

How do I maximize my deductions and credits?

To maximize your deductions, you’ll have to have expenses in the following IRS-approved categories:

- Medical and dental expenses.

- Deductible taxes.

- Home mortgage points.

- Interest expenses.

- Charitable contributions.

- Casualty, disaster and theft losses.

What do tax credits exemptions and credits encourage?

Tax exemptions, deductions, and credits all can reduce the amount of taxes that a person owes. Some of these tax benefits are intended to reflect a person’s ability to pay tax; the Child Tax Credit, for example, recognizes the costs of raising children.

Are tax credits or deductions better?

Tax credits are generally considered to be better than tax deductions because they directly reduce the amount of tax you owe. If you’re in the 10% tax bracket, for example, a $1,000 deduction would only reduce your taxable income by $100 (0.10 x $1,000 = $100).

How are tax credits and deductions help you?

Deductions can reduce the amount of your income before you calculate the tax you owe. Find credits and deductions for businesses. Claim certain credits your tax return and you may be able to get a larger refund, while others may give you a refund even if you don’t owe any tax.

When do you claim credits on your tax return?

You can claim credits and deductions when you file your tax return. Tax credits and deductions can change the amount of tax you owe so you pay less. Credits can reduce the amount of tax you owe. Deductions can reduce the amount of your income before you calculate the tax you owe. Find credits and deductions for businesses.

Are there any tax deductions that low income people can claim?

Low-income taxpayers can deduct up to 50% of their contributions to a SIMPLE, SEP, traditional or Roth IRA, 401 (k), 403 (b), governmental 457 (b) plan, or ABLE account. The maximum saver’s credit available is $4,000 for joint filers and $2,000 for all others. Use Form 8880 and Form 1040 Schedule 3 to claim the saver’s credit.

Are there any tax deductions you can take in 2020?

While few people want to pay anything at all, there are ways to pay less. Tax deductions and tax credits can help you save money in tax season 2020. Deductions lower your taxable income (and reduces your tax burden), while tax credits are a dollar-for-dollar reduction to your tax bill.