A negative capital account is a partnership tax concept describing the situation in which adjusted basis in partnership assets is less than the outstand- ing debt of the partnership. When the capital account is negative, the partnership is a tax shelter, worth more after tax than in the absence of tax.

Can an LLC have a negative capital account?

Partners and members of an LLC taxed as a partnership will often have negative or deficit capital account balances at the end of a taxable year. A negative capital account balance is permissible if supported by proper allocation of partnership debt (or an obligation to restore a deficit).

Do distributions reduce capital account?

Distributions – Decreases capital account and outside basis. Distributive share of income and loss – Increases/decreases capital account and outside basis. Partnership liabilities – Does not affect capital account, increases/decreases outside basis.

When does a partner have a negative capital account?

A partner’s tax basis capital account can be negative if a partnership allocates tax losses or deductions or make distributions to the partner in excess of the partner’s tax basis equity in the partnership, or when a partner contributes property subject to debt in excess of its

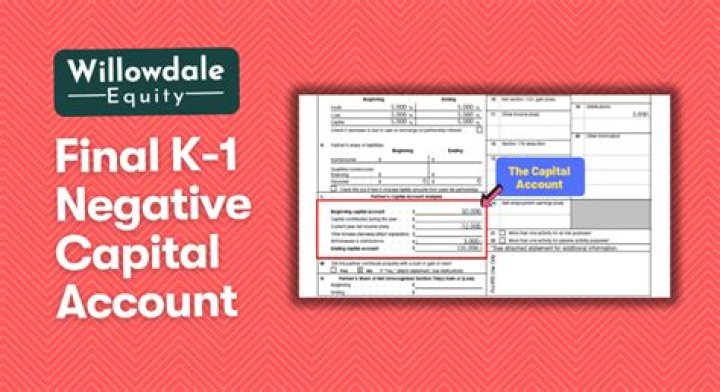

Can you have a negative capital account on k 1?

A partner’s tax basis capital account can be negative if a partnership allocates tax losses or deductions or make distributions to the partner in excess of the partner’s tax basis equity in the partnership, or when a partner contributes property subject to debt in excess of its adjusted tax basis to a partnership. Click to see full answer.

When does a partnership have negative tax basis?

Negative “tax basis capital” generally exists when a partnership allocates tax deductions or losses or makes distributions to a partner in excess of the partner’s tax basis equity in the partnership. It can also arise when a partner contributes property subject to debt in excess of the property’s adjusted tax basis to a partnership.

How to report negative tax basis capital accounts?

How do I report a partners’ negative tax basis capital accounts on a partnership return?