That is the number you will put in the 982 form under insolvency and goes with your return. If your insolvency is greater than your canceled debt, you have no canceled debt will not be taxable.

Do you have to include Form 982 on your tax return?

That is the number you will put in the 982 form under insolvency and goes with your return. If your insolvency is greater than your canceled debt, you have no canceled debt will not be taxable. I recommend mailing in the return to include both form 982 and the worksheet.

Can you use Form 982 to cancel debt?

Unnecessary given that the potential income and tax bill resulting from this cancelled debt will be eliminated using Form 982. Taxpayers with cancelled debt scenarios should be wary of self-preparing their tax returns.

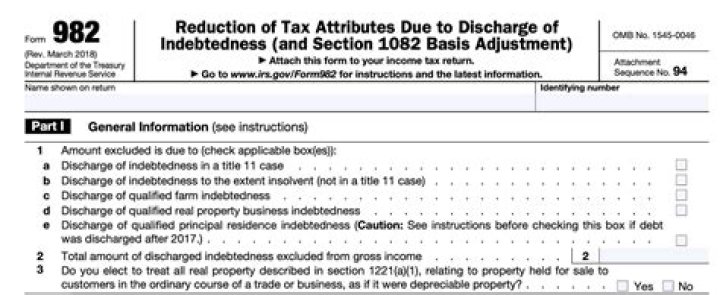

What does discharge of indebtedness mean on IRS Form 982?

Discharge of Indebtedness. The term discharge of indebtedness conveys forgiveness of, or release from, an obligation to repay. File Form 982 with your federal income tax return for a year a discharge of indebtedness is excluded from your income under section 108 (a).

Can you exclude discharged indebtedness on Form 982?

However, under certain circumstances described in section 108, you can exclude the amount of discharged indebtedness from your gross income. You must file Form 982 to report the exclusion and the reduction of certain tax attributes either dollar for dollar or 33 1 / 3 cents per dollar (as explained later).

What does qualified acquisition indebtedness mean on IRS Form 982?

Qualified acquisition indebtedness is (a) debt incurred or assumed to acquire, construct, reconstruct, or substantially improve real property that is secured by such debt and (b) debt resulting from the refinancing of qualified acquisition indebtedness to the extent the amount of such debt doesn’t exceed the amount of debt being refinanced.

How are assets classified in statement of affairs of insolvent?

The assets as shown in the statement of affairs of insolvent are classified into the four categories as follows − Property as per List E − Other than the bills receivable in hand and the assets as kept by creditors as fully and partly secured debts are comes under this list.

How to estimate asset values for insolvency and..?

IRS Publication 4681 (link opens PDF) includes an insolvency worksheet on page 8, which lists the assets you need to value. These include: Investments in collectibles (coins, stamps, etc.)

Do you have to file Form 982 when debt is discharged?

When an individual has a debt that has been discharged, the amount that was discharged is generally treated as taxable income to the individual. Under certain circumstances, this amount can be excluded from income, and therefore not taxed. In order to report the exclusion, the taxpayer must file Form 982 with their tax return.

What is the form for the insolvency exemption?

Publication 4681 provides detailed instructions for completing Form 982 — affectionately called “The Tax Form from Hell” due to its byzantine complexity. Form 982 is the document you include with your Federal Form 1040 to claim the insolvency exemption.

Can a unpaid bill be a sign of insolvency?

Yes, being unemployed and having unpaid bills is definitely a sign of insolvency. Basically, if you were “insolvent” prior to getting the debt relief that generated the form 1099-C, then the debt would be excluded from income using the form 982. Here is a link to the IRS discussion of “insolvency”.

What do you need to know when you are insolvent?

You will need to see what your bank account, credit card debts, car debt, house debt, etc. were on that date (unpaid medical expenses, etc.) If your llabilities are greater than your assets, (do not include the debt amount canceled), you are insolvent.

When does the insolvency exclusion apply in Title 11?

The insolvency exclusion doesn’t apply to any discharge that occurs in a title 11 case. It also doesn’t apply to a discharge of qualified principal residence indebtedness (see Line 1e, later) unless you elect to have the insolvency exclusion apply instead of the exclusion for qualified principal residence indebtedness.