A form 1099-S is a tax document used to ensure that the full amount received for a real estate sale of some kind is accurately reported. When real estate is sold, the seller is often subject to a capital gains tax. A 1099-S can also be used to report income made on rental property or investment property.

Do you have to file a 1099 when selling real estate?

When real estate is sold, the seller is often subject to a capital gains tax. A 1099-S can also be used to report income made on rental property or investment property. For selling real estate, the buyer must complete and file their own 1099-S. Buyers can ask for a 1099-S to be completed and included as part of their closing documents.

What happens if you dont report a 1099-S to the IRS?

If the business or other party involved in the real estate transaction submits a 1099-S form to the IRS, as they are required to do by law and a taxpayer does not report it, the IRS will likely send a bill for taxes owed on the income.

When to use IRS Form 1099 for closing?

IRS Form 1099-S is an important (and often overlooked) step in the closing process for real estate transactions that are closed in-house.

Why are some 1099’s not taxable to payee?

For a variety of reasons some Form 1099 reports may include amounts that are not actually taxable to the payee. A typical example is Form 1099-S for reporting proceeds (not gain) from real estate transactions. The Form 1099-S preparer will report the sales proceeds without regard to the amount of the taxpayer’s “basis” in the real estate sold.

Where do I Find my 1099s for real estate?

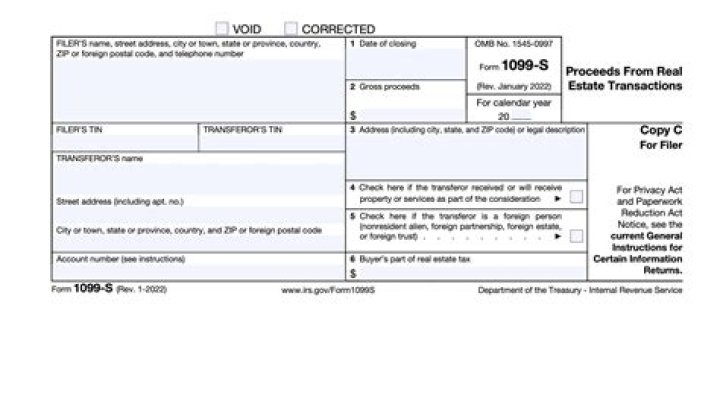

If you received your 1099-S for the sale of a business or rental property, this is reportable on IRS Form 4797 and Schedule D. A 1099S form contains information about the Filer, the Transferor, the Date of Closing, Proceeds, and details of the property being transferred.

When did the IRS start using Form 1099?

Note that for those who have electronic filing of Form 1099 set up, the due date for the IRS is March 31 rather than the last day of February. In 1918, Form 1099 was created by the Internal Revenue Service for use with the 1917 tax year. At the time, employers were required to use the form to report salaries paid in excess of $800.