The statement of cash flows classifies cash receipts and disbursements as operating, investing, and financing cash flows. Both inflows and outflows are included within each category. Look at Exhibit 2 to see how activities can be classified to prepare a statement of cash flows.

Which item must be first item for prepare statement of cash flow under indirect method of operating activity?

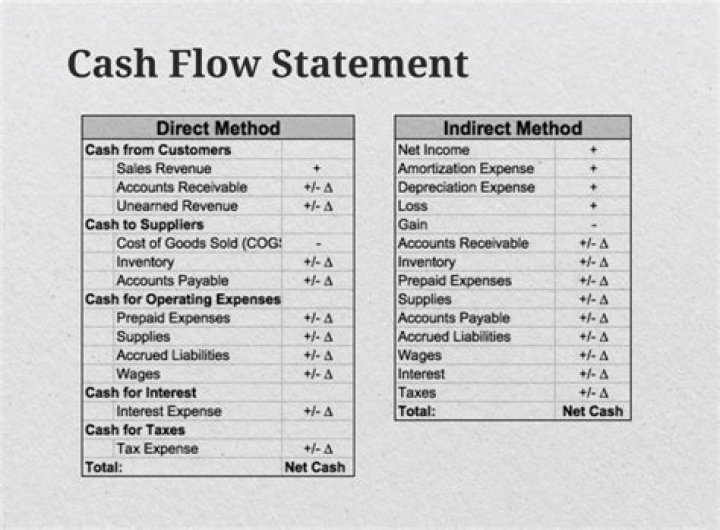

Under the indirect method, cash flow from operating activities is calculated by first taking the net income from a company’s income statement.

What are the three classifications of the statement of cash flows?

The statement of cash flows presents sources and uses of cash in three distinct categories: cash flows from operating activities, cash flows from investing activities, and cash flows from financing activities.

How do you do an indirect cash flow statement?

Prepare the Operating Activities Section of the Statement of Cash Flows Using the Indirect Method

- Begin with net income from the income statement.

- Add back noncash expenses, such as depreciation, amortization, and depletion.

- Reverse the effect of gains and/or losses from investing activities.

How do you prepare an indirect cash flow statement?

What is indirect method of cash flow statement?

The indirect method presents the statement of cash flows beginning with net income or loss, with subsequent additions to or deductions from that amount for non-cash revenue and expense items, resulting in cash flow from operating activities.

What is the difference between direct and indirect method of cash flow statement?

The main difference between the direct and indirect cash flow statement is that in direct method, the operating activities generally report cash payments and cash receipts happening across the business whereas, for the indirect method of cash flow statement, asset changes and liabilities changes are adjusted to the net …

What is an indirect cash flow statement?