The earnings limit does not apply if you file for benefits at your full retirement age or beyond. These limits only apply to those who begin taking Social Security benefits before reaching full retirement age. The earnings limit is an individual limit.

How old do you have to be to use social security quick calculator?

So benefit estimates made by the Quick Calculator are rough. Although the “Quick Calculator” makes an initial assumption about your past earnings, you will have the opportunity to change the assumed earnings (click on “See the earnings we used” after you complete and submit the form below). You must be at least age 22 to use the form at right.

How much does social security pay at age 65?

Social Security may provide $33,773. If you start collecting your benefits at age 65 you could receive approximately $33,773 per year or $2,814 per month. This is 44.7% of your final year’s income …

How much Social Security income is considered taxable income?

Photo credit: © iStock/Kameleon007. If you have a lot of income from other sources, up to 85% of your Social Security benefits will be considered taxable income. If the combination of your Social Security benefits and other income is below $25,000, your benefits won’t be taxed at all.

What happens if you file for Social Security at 62 instead of 67?

If you claim benefits earlier than FRA, you get smaller checks, but you should get them for a longer period of time. For example, if you claim benefits at 62 instead of 67, you get five additional years of income from the SSA — or a total of 60 more monthly checks than if you had waited to claim at 67.

How much money do you get if you file early for Social Security?

This shows you’d need to receive the extra $326.62 for about 144 months (12 years) to break even for delaying. It would take you a total of 12 years of receiving a higher monthly benefit to make up for waiting from 62 to 66 to start getting monthly Social Security benefits.

How does the Social Security quick calculator work?

Social Security Quick Calculator. Benefit estimates depend on your date of birth and on your earnings history. For security, the “Quick Calculator” does not access your earnings record; instead, it will estimate your earnings based on information you provide.

What happens if my Social Security income exceeds$ 44, 000?

If your income exceeds $44,000, up to 85% of your benefits could be taxable. If you are married filing separately, it is a little more complicated and you could end up paying taxes on up to 85% of your benefit. What is “combined income”?

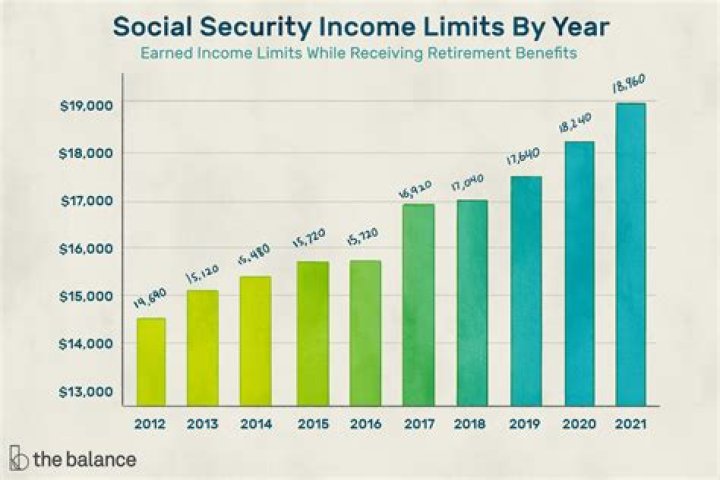

What’s the income limit for Social Security for 2020?

For 2020, the limit is $18,240. For every $2 you exceed that limit, $1 will be withheld in benefits. The exception to this dollar limit is in the calendar year that you will reach full retirement age.

What’s the income limit for Social Security in 2015?

The annual limit in 2015 and 2016 is $15,720. The rules are more lenient beginning in January of the year you reach full retirement age. Up until your birthday month, Social Security will deduct $1 of your benefit payments for every $3 you earn above $41,880.

Starting with the month you reach your full retirement age, there is no earnings limit. Your work income has no effect on the amount of your benefits. Keep in mind. Social Security can only use the special monthly rule in one calendar year. Starting the next year, income-related deductions from benefits are based solely on your annual earnings.

What happens to your Social Security benefits when you retire?

I had additional earnings after I retired; will my monthly Social Security retirement benefit increase? Each year we review the records for every working Social Security beneficiary to see if the additional earnings will increase their monthly benefit amounts.

When does Social Security have to be included in gross income?

There are certain situations when seniors must include their Social Security benefits in gross income. If you are married but file a separate tax return and live with your spouse at any time during the year, then all of your Social Security benefits are considered gross income which may require you to file a tax return.

Do you have to pay taxes on Social Security income?

your gross income is $14,050 or more. However, if you live on Social Security benefits alone, you don’t include this in gross income. If this is the only income you receive, then your gross income equals zero, and you don’t have to file a federal income tax return.

When do senior citizens have to file taxes?

Married seniors above the age of 65 filing joint returns must file taxes if their combined income is $23,100 or higher.

What are the Social Security benefits at age 62?

Full Retirement and Age 62 Benefit By Year Of Birth Year of Birth 1. Full (normal) Retirement Age Months between age 62 and full retiremen At Age 62 3. At Age 62 3. 1958 66 and 8 months 56 $716 33.33% 1959 66 and 10 months 58 $708 34.17% 1960 and later 67 60 $700 35.00%

Why is Social Security the sole source of income for older Americans?

En español | Social Security was never designed to be the sole source of income for older Americans. But in an era of disappearing pensions, dwindling savings and longer life spans, it has become the primary, and at times the only, financial lifeline for some.

What’s the maximum amount a family member can get from Social Security?

Children who are under age 19 or disabled may also qualify for benefits based on your work record. The maximum family benefit all your family members can receive is usually about 150% to 180% of your full retirement benefit.

Is the Government Pension Offset included in SSA benefits?

Your benefit may be offset by the Government Pension Offset (GPO). Get the most precise estimate of your retirement, disability, and survivors benefits. The estimate includes WEP reduction.