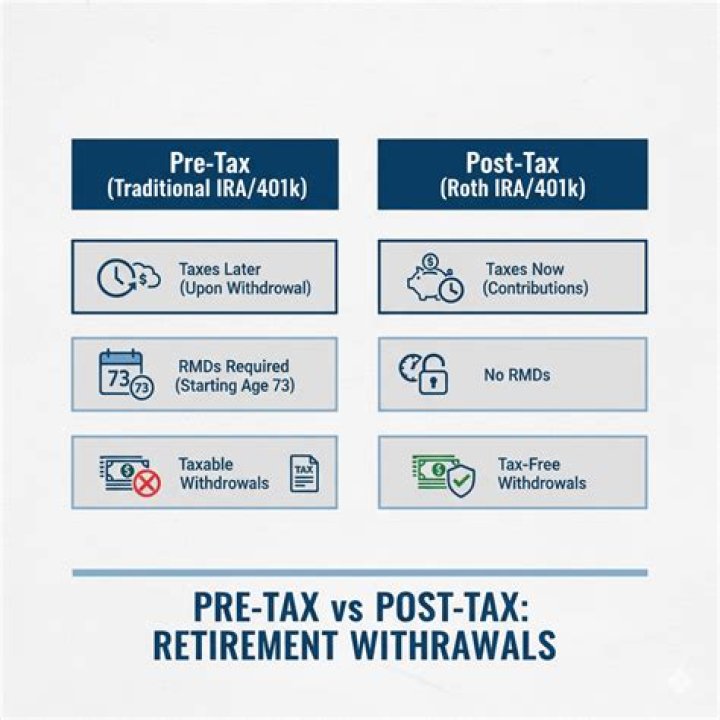

A Traditional IRA is an Individual Retirement Account to which you can contribute pre-tax or after-tax dollars, giving you immediate tax benefits if your contributions are tax-deductible.

Does traditional IRA use post tax dollars?

Qualified plan to traditional IRA: All rollover-eligible amounts can be rolled over to a traditional IRA. This includes after-tax amounts. Qualified plan to qualified plan: All rollover-eligible amounts can be rolled over to another qualified plan, provided the plan allows it.

Are after tax contributions to IRA tax-deductible?

Are IRA contributions tax-deductible? Yes, IRA contributions are tax-deductible — if you qualify. To be clear, we’re talking here about contributions to a traditional IRA. Contributions to a Roth IRA are not tax-deductible.

How are IRA deductions taxed?

Contributions to traditional IRAs are tax-deductible, earnings grow tax-free, and withdrawals are subject to income tax. Early withdrawals (before age 59½) from a traditional IRA—and withdrawals of earnings from a Roth IRA—are subject to a 10% penalty, plus taxes, though there are exceptions to this rule.

Do you get a tax deduction for IRA contributions?

Taxpayers can deduct contributions to a traditional IRA if they meet certain conditions. If the taxpayer or their spouse was covered by a retirement plan at work, the deduction may be reduced or phased out. This reduction goes until the deduction is eliminated.

Is there a phase out of the IRA deduction?

For anyone who is covered by an employer-sponsored retirement plan, the deduction has a phase out and your income will determine whether all, some, or none of your IRA contribution is deductible. The value of your IRA deduction depends on four main factors:

How is the post tax portion of an IRA contribution calculated?

Rather, withdrawals are a mix of pre-and post-tax dollars. IRS Form 8606 is used to calculate the taxable portion of a distribution from a traditional IRA that has post-tax dollars. The post-tax dollars included in each distribution reduce the IRA’s basis.

What are some of the post tax deductions?

Common post-tax deductions include: 1 Some retirement plans (such as a Roth 401 (k) plan) 2 Disability insurance 3 Life insurance 4 Garnishments More …