Interest is classified by the way loan proceeds are used. For instance, if loan proceeds are used to buy investment property or business property, the interest paid is classified as investment interest or business interest.

What is a business interest?

A business interest is the involvement of an individual or their family members in any trade or profession, along with any direct interest they may have in any company providing goods or services to the school. For example, if a Governor runs their own building company or provides training courses for teaching staff.

What are business interest limitations?

Business Interest Expense Limitation. A taxpayer may deduct interest paid or accrued within a tax year on a valid debt. Prior to the Tax Cuts and Jobs Act of 2017 (TCJA), business interest expense was generally deductible in the year the interest was paid or accrued, subject to certain limitations.

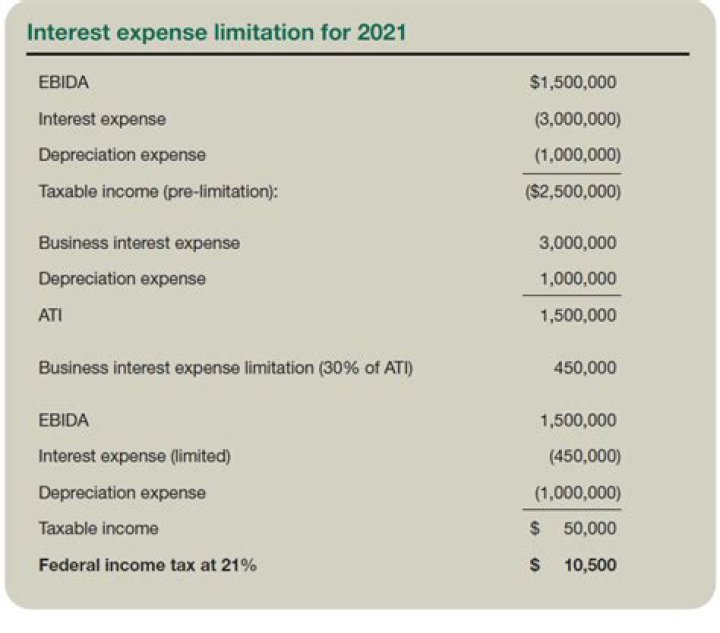

What’s the new limit for business interest expense?

The TCJA now limits deductions for business interest expense to an amount that is equal to interest income plus 30 percent of the taxpayer’s adjusted taxable income (essentially EBITDA through 2021, thereafter EBIT). Any business interest expense that exceeds the new Section 163 (j) limit is carried forward indefinitely.

What do you not deduct for business interest expense?

The deduction limitation for taxable income does not take into account business interest expenses and income, net operating losses, non-business income (like gains from assets that were held as investments), and depreciation, amortization or depletion.

When do you have to pay interest on trader funds?

However, effective for tax years beginning January 1, 2018, the interest expense for the material participant in a trader fund could be limited to 30% of the business’ adjusted taxable income under the Tax Cuts and Jobs Act of 2017 (“TCJA”).

Where does interest expense go on a tax return?

Breaking Down Business Interest Expense. Business expenses must be deducted on the proper tax form that correlates to the business for which the expenditure was made. Taxpayers who incur corporate business expenses cannot deduct this expense on their returns.