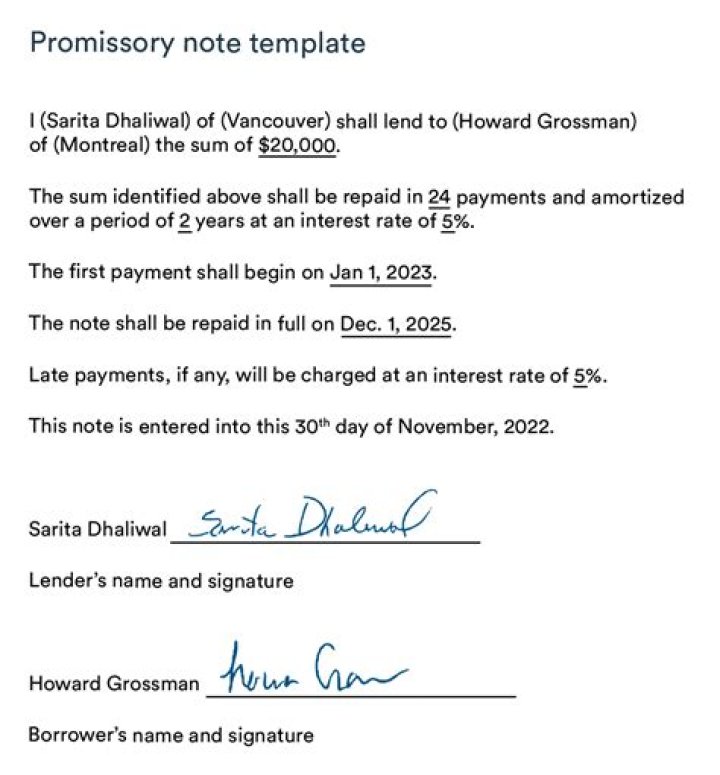

A promissory note is a financial instrument that contains a written promise by one party (the note’s issuer or maker) to pay another party (the note’s payee) a definite sum of money, either on demand or at a specified future date.

Is a promissory note a liability to the payee?

A promissory note is incomplete until delivered to the payee or bearer. primary liability for its fulfilment and endorsers have secondary liability. The BEA provides that where the note includes the words “I promise to pay” and is signed by more than one party, then liability is deemed to be joint and several.

Who is the payee on a promissory note?

Definition: A note payee, or payee of the note, is the person or entity whom the note is payable. In other words, a payee is the person who the note is made to. I remember it like this. The payee is the person who gets paid.

What is the limit for promissory note?

All Promissory Notes are valid only for a period of 3 years starting from the date of execution, after which they will be invalid. There is no maximum limit in terms of the amount which can be lent or borrowed. The issuer / lender of the funds is normally the one who will hold the Promissory Note.

Who holds a promissory note?

The lender holds the promissory note while the loan is outstanding. When the loan is paid off, the note is marked as “paid in full” and returned to the borrower.

How long does a promissory note last?

Depending on which state you live in, the statute of limitations with regard to promissory notes can vary from three to 15 years. Once the statute of limitations has ended, a creditor can no longer file a lawsuit related to the unpaid promissory note.

Does a promissory note stand up in court?

Promissory notes are a valuable legal tool that any individual can use to legally bind another individual to an agreement for purchasing goods or borrowing money. A well-executed promissory note has the full effect of law behind it and is legally binding on both parties.