two years

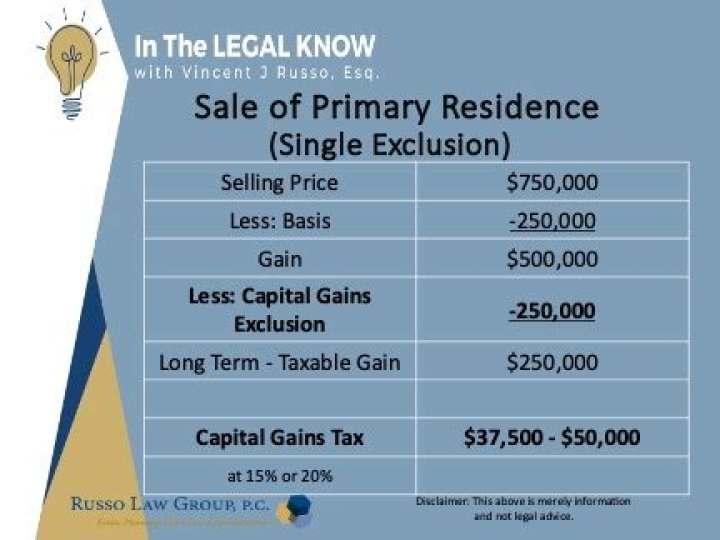

If you’ve owned your home for at least two years and meet the primary residence rules, you may owe tax on the profit if it exceeds IRS thresholds. Single persons can exclude up to $250,000 of the gain, and married persons filing a joint return can exclude up to $500,000 of the gain.

How often can you use 121 exclusion?

While homeowners can claim this exclusion an unlimited number of times, it can only be claimed once every two years. To meet eligibility requirements, you’ll need to ensure that you don’t claim the exclusion more than once in two years.

What do you need to know about Section 121 exclusion?

Qualifying for the Exclusion. In general, to qualify for the Section 121 exclusion, you must meet both the ownership test and the use test. You’re eligible for the exclusion if you have owned and used your home as your main home for a period aggregating at least two years out of the five years prior to its date of sale.

How much can you exclude from the primary residence exclusion?

You can only exclude 50% of your gain, i.e., $100,000, because 50% of the years before the sale are considered nonqualified for the exclusion since during those years the home was not used as a primary residence.

Can a home qualify for a partial exclusion of gain?

To qualify for a partial exclusion of gain, meaning an exclusion of gain less than the full amount, you must meet one of the situations listed in Does Your Home Qualify for a Partial Exclusion of Gain, later. Before considering the Eligibility Test or whether your home qualifies for a partial exclusion, you should consider some preliminary items.

What are the income limits for IRC Section 121?

The core of IRC section 121 is fairly simple. Individual homeowners can exclude from gross income up to $250,000 of gain ($500,000 for certain married couples filing jointly) provided that they satisfy the ownership requirements.