In the case of a non-SSTB, when taxable income exceeds the threshold amount, the QBI deduction is calculated by taking the lesser of:

- 20% of QBI; or.

- The greater of: 50% of the W-2 wages; or. The sum of 25% of the W-2 wages plus 2.5% of the UBIA of all qualified property.

Does Qbi reduce taxable income?

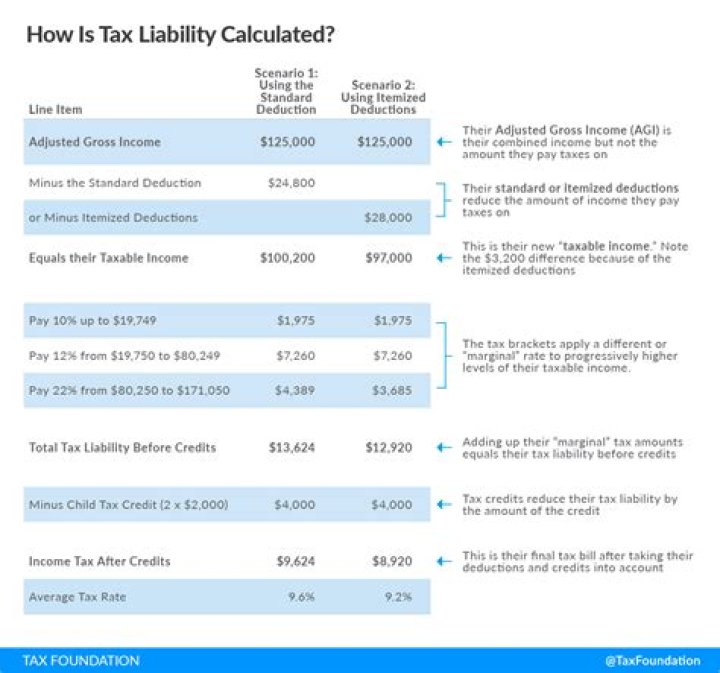

The deduction is taken “below the line,” i.e., it reduces your taxable income but not your adjusted gross income. But it is available regardless of whether you itemize deductions or take the standard deduction.

Why am I not getting the Qbi deduction?

The reason you may not receive a full 20% of QBI deduction is because the overall deduction cannot exceed 20% of your taxable income after subtracting out capital gains. As explained above, being considered an SSTB does not matter if your taxable income is below $315,000.

How much income do you have to have to claim QBI?

Eligibility. If your joint taxable income is under $315,000, you can take the full QBI deduction. If your joint taxable income is over $415,000, your deduction depends upon the wages paid by your business or the assets owned by the business. If you fall between the $315,000 and $415,000, the deduction is between the full amount and…

Is the qualified business income QBI deduction dependent on form of business?

However, simply having your company organized as one of these entities for tax purposes does not necessarily mean you will be eligible for the deduction. In addition to the limitation on the form of business, the QBI deduction is also dependent upon the nature of your business.

How is the QBI deduction calculated for SStB?

Step 4: If your business is an SSTB with income in the phase-out range, you’ll calculate your deduction by taking 20 percent of your qualified business income and applying the limitation of: Compare these calculations to 20 percent of your QBI and deduct the smaller amount.

When to use publication 535 for QBI deduction?

Use the worksheet in the Form 1040 instructions if your taxable income before the QBI deduction isn’t more than $157,500 ($315,000 if married filing jointly). Use the Publication 535 worksheet if your taxable income before the QBI deduction is higher than that threshold.