The amount of the AAA allocated to each distribution is determined by multiplying the balance of the AAA at the close of the current taxable year by a fraction, the numerator of which is the amount of the distribution and the denominator of which is the amount of all distributions made during the taxable year.

How do I pay my S corp distribution?

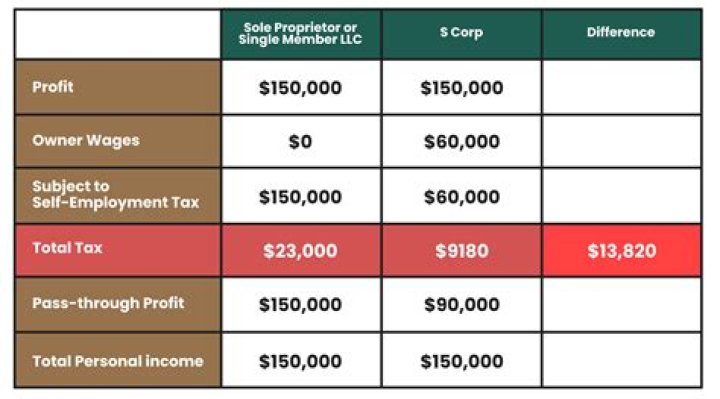

Here’s a simple strategy that you can try, and it’s called the 60/40 rule:

- Pay 60% of your business income to yourself in the form of employee salary.

- Pay yourself 40% of your business income in the form of distributions.

What are rules for adjustments to S corporation basis?

Sec. 1367 provides rules for adjustments to S corporation shareholders’ basis in their stock. Generally, basis is increased for items of income (including tax-exempt income) and the excess of deductions for non–oil and gas depletion over basis of the property subject to depletion.

Which is the basis schedule of a corporation?

“Back to Basis”- Basis Schedule of S Corporation Box 1 Ordinary Business Income (loss) (8,000) Box 2 Rental Income 4,000 Box 4 Interest Income 2,000 Box 9 Net Section 1231 Gain (Loss) 1,900 Box 16A Tax Exempt Interest * 500

How does income affect S corporation stock basis?

Unlike with C corporation stock basis, which stays the same each year, annual income, distributions and loans can all affect an S corporation shareholder’s basis, in sometimes surprising ways.

Where to find basis on Form 1040 for S corporation?

“ As stated in Part II of the Schedule E (Form 1040), a taxpayer who owns an interest in an S corporation and reports a loss, receives a distribution, disposes of stock, or receives a loan repayment from the S corporation must check a corresponding box under line 28, column (e), and attach a computation detailing their S corporation basis.